It's Busy Out There

We live in busy and interesting times, that’s for sure. Take the last week or so as an example. All at once we had the impeachment trial in the Senate, Brexit looming (it happened last Friday, by the way), and the coronavirus outbreak in China. We also had some strong but contradictory economic numbers percolating too.

But it was China that tended to dominate the market’s attention, especially last Friday when the Dow Jones Industrial Average slid 600 points, or a little over 2%. The S&P 500 fared a bit better but both indexes ended the volatile week down 2% or so. The main emerging markets index (of which China is a large portion) was down over 5% for the week.

Due to the outbreak the Chinese government had extended holiday closures of local stock markets through last week. Here at home risk associated with the virus had largely been priced into our markets since we weren’t on holiday. But investors in China hadn’t yet had an opportunity to “trade” the situation. As soon as they did yesterday, they sold, sending stocks in China down about 8%, an impressive single-day decline for any country. This let Chinese stocks catch up with commodities like oil, for example, which have been in freefall on fears that the outbreak will cause Chinese demand to slow.

The week of market turmoil also caused the yield curve here at home to invert… again. Although the inversion was slight, it’s still technically a recession indicator. The inversion has since reversed as of this writing as fears about coronavirus dissipate and investors sell bonds to buy more stocks. Still, the bond market has taken notice and currently expects one or two interest rate reductions from the Fed this year.

Fortunately for markets the outbreak came at a time when some of our economic indicators have been turning positive. The Institute for Supply Management tracks manufacturing activity across the country. The index had been contracting for several months but showed a surprise uptick in January, rising from 47.2 to 50.9. Readings below 50 indicate a recession for the sector, so this is a positive change after being weak for a while.

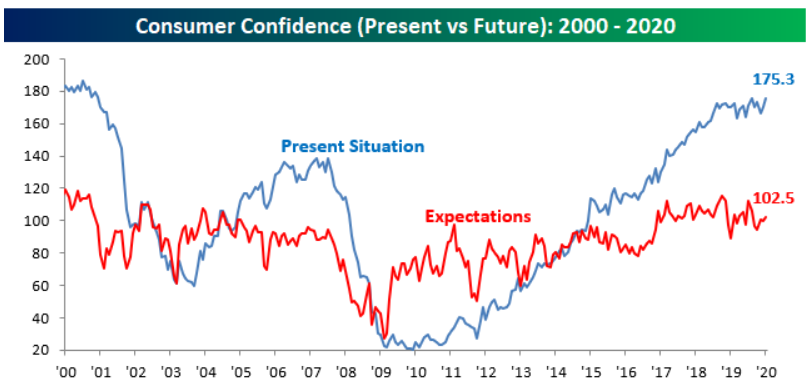

We also learned last week that consumer confidence has continued to rise well above its long-term average. Interestingly, at the same time consumers are reporting optimism, they’re also feeling less confident about their prospects. Your guess is as good as mine in terms of explaining this dichotomy, but it seems like a negative if one feels satisfied today yet doesn’t think it will last. That has to start showing up in our consumer-driven economy at some point, right?

While our economy seems to be trucking right along and defying gravity a bit, and markets have snapped back from last week’s losses, more short-term volatility should be expected as issues like coronavirus and Brexit play out in coming weeks. As we’ve seen in recent years, volatility bursts back onto the scene at unexpected times and in unanticipated ways. It’s important to remember that sometimes the best thing to do about market turmoil is absolutely nothing.

Have questions? Ask me. I can help.

- Created on .