What’s with Emerging Markets?

A common topic lately has been the problems with emerging markets and why the asset class is down so much this year. It's important for investors to examine these problems because the asset class is expected to generate excess returns over time but is underperforming now. We know we're supposed to "buy low and sell high", but in practice it's a very hard thing to do, especially when it comes to more complicated parts of the global stock markets.

Let's define what we mean by "emerging markets", or EM. Technically speaking, EM is an asset class driven by a major index provider, Morgan Stanley Capital International (MSCI). The firm maintains the primary index meant to represent stock markets around the world not including developed markets such as the U.S., Europe, and Japan.

Currently, 33% of the index is made up of Chinese companies, with the next largest weightings being South Korea at 15%, India at about 9%, and Brazil and South Africa at around 7% each. The remainder of the index is spread across the rest of the developing world, including countries like Turkey (about a 1% weighting) whose currency woes have made news recently.

Over time the index, and the funds that track it closely, have performed well. This outperformance is expected to continue. Compared with growth assumptions for U.S. stocks of about 6.5 – 7.25% on average over the next ten or so years, EM is expected to grow by 8.25%.

But higher expected returns come with higher expected volatility. Just as with the bonds versus cash debate from last week, or any publicly traded investment versus cash for that matter, you're going to have to endure periods of underperformance if you want greater return potential over time.

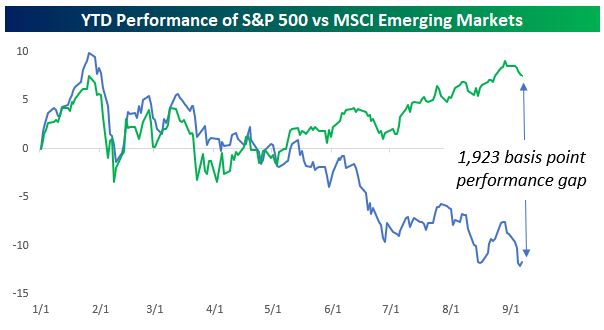

After a solid year in 2017, EM is down almost 10% year-to-date and has fallen just a hair over 20% from the index's high in late-January, as seen in the following chart from Bespoke Investment Group (1,923 basis points is 19.23%, by the way). This performance stands in stark contrast to U.S. indexes that have returned almost 9%, 12%, even 15% so far this year. What caused this reversal in EM performance?

Continue reading...

The answer to this question is complicated and I don't pretend to be an expert in all its aspects. Primarily, the issue has to do with investor sentiment around U.S. trade policy (tariffs), but a close second has to do with something more nebulous: currency exchange rates. The dollar has been climbing versus other foreign currencies and is causing upheaval in many emerging economies.

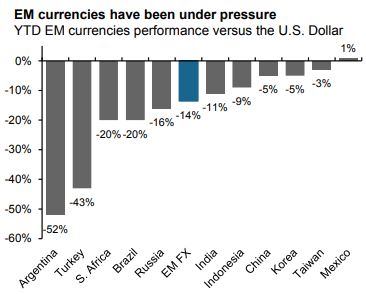

The U.S. dollar is the global standard when it comes to trade and payments, and many emerging economies have borrowed heavily in dollars. The issue is that borrowers usually have to convert their own currency into dollars to pay back the loans. This isn't a problem if the local currency is stable compared with the dollar or maybe the borrower has a healthy stash of dollars to draw from. But throw in a declining currency and a dwindling supply of dollars, and things can turn ugly.

Think of it this way. Imagine you borrowed $1,000 in January but the only cash you have available is from a recent trip you took to Argentina. Paying back the loan in pesos now would cost nearly twice as much as when you took out the loan, quickly doubling your debt level. This obviously has broad implications in your financial life. Maybe you're forced to reduce spending in other areas to pay back the debt. Or, maybe you simply can't pay it back at all.

Extend this to the corporate or national level (adding some zeroes, of course) and you get a sense of the potential problem. The following chart, courtesy of JPMorgan, shows how various emerging market currencies have fared versus the dollar this year.

We know from the MSCI weightings previously referenced that countries with the worst currency performance this year are also some of the smallest in the index. This contains risk, in a sense, for us here in the U.S. Additionally, at this point most analysts don't think the problem will spill over to our shores and this is playing out as relative outperformance in our stock market. But it's a problem nonetheless, so what's a long-term investor to do?

As I've mentioned previously, EM is expected to be a growth engine over the long-term. But the asset class is also expected to be the most volatile in your portfolio.

In general, investors still want this exposure but only in relatively small amounts, such as perhaps 3-5% of one's diversified portfolio, depending on one's goals and risk tolerance. The idea is to come up with a weighting for emerging markets, say 4%, and then rebalance back to that amount as the asset class grows (or declines) around that threshold.

Sticking to this kind of process over the long-term is preferable to trying to chase market performance, which is complicated in the extreme even before issues like currency risk come into play.

Here's a link to MSCI's page for it's EM index if you'd like to read more.

https://www.msci.com/emerging-markets

Have questions? Ask me. I can help.

- Created on .