In recent weeks we’ve talked about how investor expectations around the Fed and interest rates have helped disturb markets this quarter. Just last week the “Magnificent Seven”, large and popular tech stocks including Nvidia and Microsoft, collectively dropped almost a trillion dollars in market value, a record dollar amount for that timeframe. The dollar decline is that high because those companies have grown so much lately and even a relatively benign percentage drop comes off a larger number, but it’s still a noteworthy chunk of money.

Beyond news like that, consternation has been growing for some investors as we get deeper into election year politics and questions about the Fed and potential ulterior motives for its rate decisions get thrown into the mix. The Fed itself, as explained numerous times by none other than its chairperson, Jerome Powell, is an apolitical organization. They have two jobs given to them by Congress – keep inflation manageable and foster a strong labor market. Dabbling in politics isn’t their third responsibility. This has been reiterated countless times over the years but questions still remain.

Does the Fed play politics? Do they raise rates to punish or reduce rates to play favor? Do voting members of the Fed’s rate-setting committee put their collective thumb on the scale for specific candidates, political parties, or their personal agendas?

These are valid questions but, as with the politicization of seemingly everything these days, answers seem open to wide interpretation. For the Fed it’s absolutely a case that anything they do, even doing nothing at all, will be second-guessed and derided by many. So instead of getting overly political, which is something I wholeheartedly try to avoid in these posts, let’s look at some data and analysis on this topic compiled by my research partners at Bespoke Investment Group.

From Bespoke…

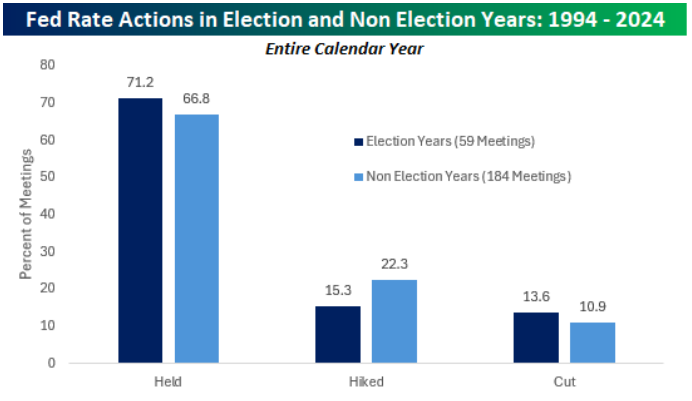

In looking at Fed policy actions since 1994 during election and nonelection years, on a net basis, the Fed was more likely than normal in an election year to keep rates on hold, less likely to hike, and more likely to cut rates.

The only election year that the Federal Reserve cut rates in the period from May through November was in October 2008 when the financial system was on the brink of collapse and neither candidate was an incumbent.

It’s hard to imagine any aspect of society as not having a political view these days, especially in Washington DC. If there’s one institution that has mostly managed to stay out of the political fray, though, it’s the Federal Reserve. Individual members have their political biases and some former members even find their way to serve in the administration of the President, but in formal communications and in their official capacities, they tend to stay out of politics.

With 2024 being a Presidential election year, the subject of rate cuts and their timing takes on an added political twist. If the FOMC cuts rates too close to the election, they could be seen as trying to put their hands on the scale in favor of the incumbent while a rate cut right after the election could be seen as rewarding the winner and trying to give them a ‘head start’. Currently, some Democrats have already expressed concern that keeping rates too high for too long has hurt the economy and threatened President Biden’s re-election. Supporters of former President Trump argue instead that by just talking about and telegraphing rate cuts, the Fed is goosing the economy to get President Biden re-elected. Being Fed Chair sounds like fun, doesn’t it?

There are plenty of examples in the past of different administrations either jawboning or blaming the Federal Reserve for certain outcomes. In 1998, former President George H.W, Bush said in an interview that Fed Chair Greenspan’s reluctance to more forcefully lower rates during the recession of 1990-1991 resulted in the weak recovery that cost him re-election. Bush recalled “I reappointed him, and he disappointed me.”

There are always going to be stories and anecdotes to suggest whether the Fed plays politics, but the best way to look at it is through the data itself. Going back to 1994 when the Federal Reserve started announcing its rate decisions in real-time, we compared their actions (at scheduled and unscheduled meetings) in Presidential election years versus non-election years to see if there were any differences or similarities. All else equal, you would expect to see the frequency of rate hikes and cuts be the same in election and nonelection years.

The first chart below compares the frequency that the FOMC has held, hiked, and cut rates during Presidential election and non-election years. In years when there was a Presidential election, the Fed held rates unchanged at 71.2% of its meetings, hiked rates 15.3% of the time, and cut rates 13.6% of the time. While the differences were small, on a net basis, the Fed was more likely than normal to keep rates on hold, less likely to hike, and more likely to cut rates. The Fed may be independent, but historically there has been a slight bias of moving towards easier than tighter policy during an election year.

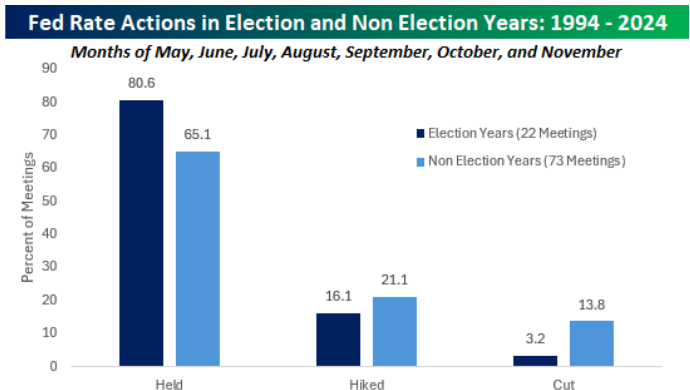

Looking more specifically, the chart below compares policy actions in May through November in election and non-election years. Here there is an even wider disparity with a bias towards sitting on their hands. At the 22 meetings during these months of Presidential election years since 1994, the Fed stayed on hold just over 80% of the time, hiked rates 16.1%, and only cut rates once (3.2%). Based on these prior actions, as the election gets closer, the Fed looks like it has historically attempted to avoid cutting rates at all costs.

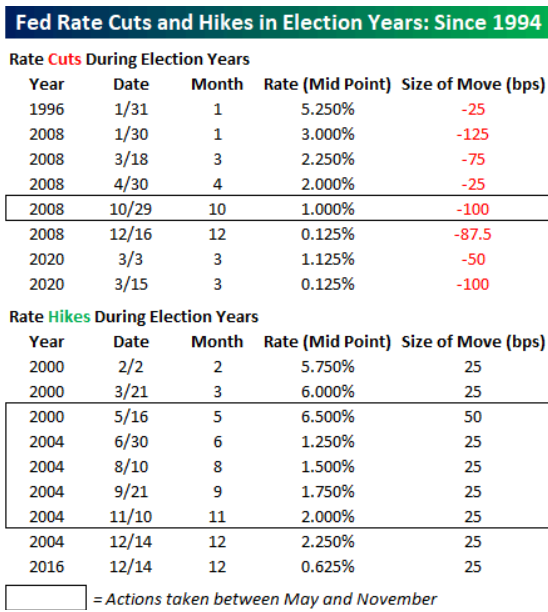

The table below shows the different times that the Fed cut and hiked rates during election years since 1994. Of the eight different rate cuts, only one occurred in the months spanning May through September, and that was a 100- bps cut on 10/29/08 when the financial system was on the brink of collapse. Not only that, but it was also an election where neither candidate was the incumbent, so politics played zero role in that example.

With regards to rate hikes during election years, five of the nine hikes occurred in 2004 when George W. Bush was running for re-election (an election he ultimately won). Besides the hikes leading up to and just after Bush II’s election in 2004, the other three hikes that occurred during election years were when neither candidate for election was an incumbent. Again, outside of that one period in 2004, the Fed appears like it prefers to stay put during election years, and as the pages of the calendar turn, it raises the question, will the rate cuts that keep getting pushed further out on the horizon ever arrive?

Have questions? Ask us. We can help.

- Created on .