Convertibles

In recent weeks we’ve been looking at bond alternatives given the asset class’s poor performance of late. As I’ve said before numerous times and in different ways, I’m not suggesting that you sell your bonds tomorrow and buy shares of an apartment building, a bunch of gold, or bitcoin. There’s no easy answer to the bond alternative question. Instead, I’m advocating for a balanced approach where you make sure your financial bases are covered before branching out into more exciting fixed income options.

It's important to remember a key benefit of bonds these days: ease of use. Since we typically access bonds via an exchange-traded index fund that usually trades for “free” within seconds, buying and selling good quality bonds is just a few clicks away. This helps make bonds a good store of cash beyond what you need to keep in the bank and what you don’t want to risk in the stock market. In other words, mostly we’re talking about bonds for the medium-term, perhaps three to ten years out. Beyond that, your savings really should be put to more productive use in the stock market, buying real estate, or perhaps even starting your own business.

Also recall that volatility risk is something to appreciate when thinking about bond alternatives. Too many investors have confused their time horizons and mismatched longer-term investments to shorter-term goals. Doing so is easy in a strong market because the rising tide effect offers lots of validation. But market mood can quickly change and that Warren Buffett quote about seeing who’s been swimming naked only after the tide has gone out can become a truism. Don’t let that be you.

(Look back at the last couple posts for a rough guide to determine how much, if any, of your bond allocation you can explore with.)

Here’s the next installment of our list of bond alternatives. I was going to include more categories this week, but this post was getting way too long. Instead, I added some extra detail regarding one category, convertible bonds. Next week we’ll look at floating rate bonds and fixed annuities.

As I mentioned previously, this list of bond alternatives isn’t meant to be exhaustive. I’m looking at investments that are relatively easy to find and buy. Also, this list should be taken as a jumping off point for your own research and not as specific investment recommendations.

Convertible Bonds –

Like preferred stocks, convertibles are a hybrid of bonds and stocks built to facilitate borrowing by companies with lower credit ratings. These companies can choose to pay higher interest rates on traditional bonds or allow bondholders the right to convert the company’s bonds into shares of company stock if the stock appreciates. This “equity kicker” allows investors to stomach buying lower quality bonds at lower interest rates. Companies of all sizes issue convertibles but smaller growth-oriented companies like this setup because money is cheaper to borrow and, assuming they grow a lot, debt can be shifted to equity over time and make room for more borrowing.

Convertibles can make sense if you’re on the fence, so to speak. After all, if you’re bullish on the company you’d just buy the stock, right? But say you like the company but also like the relative safety that comes from owning the company’s bond. If the stock appreciates you convert the bond to stock and then, presumably, sell the stock and reinvest in another convertible, sort of like flipping a house. But if the stock doesn’t appreciate, you’d hopefully earn a small amount of interest along the way to getting your principle back when the bond matures. The company could still go bust in the meantime and default on the bond, but it’s a great company with lots of potential. Seems like a win-win, right? What has ever gone wrong with circular logic?

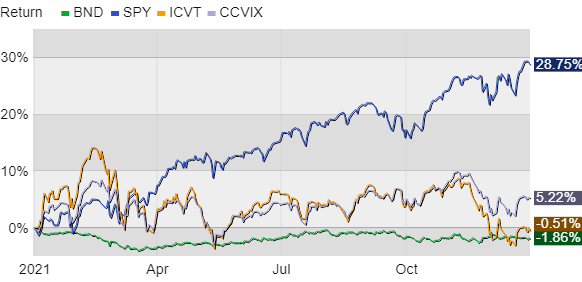

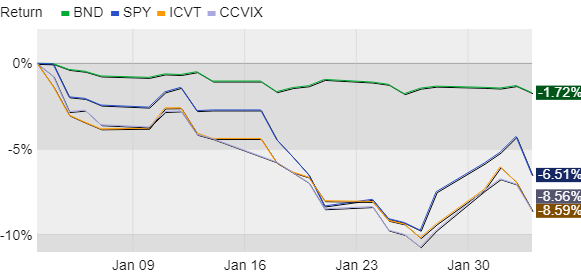

Besides the issuer risk fundamental to bonds, this is where volatility risk comes in. Convertibles lure investors with higher average returns but the catch is they’re riskier than core bonds and act more like stocks, especially during periods of uncertainty. You’ll see this playing out over two timeframes in the charts below.

The first chart is performance for all of 2021 for bonds (the green line), stocks (blue), and two popular convertible funds. The iShares Convertible Bond Fund, ticker symbol ICVT, is the orange line and the Calamos Convertible Fund, ticker symbol CCVIX, is the lavender/purple (I’m bad with colors). The second chart is the same set of investments over the past 30 days.

We see that convertibles did fine for most of last year as stocks rose. But then investors turned skittish nearing year-end and into last month. ICVT is over half invested in tech-oriented convertibles, so it really took a hit as tech faltered. The decline was nearly as swift for CCVIX, mostly for the same reason. And then in the second chart we see that both convertible funds have tracked with the stock market in the last month as volatility rose. We also see core bonds, the green line, losing ground, but to a lesser extent.

The Calamos fund performed better last year but has slightly underperformed ICVT during the past five years. This underperformance could be blamed on Calamos owning convertibles in riskier sectors of the US economy and holding less in tech, a sector that has done extremely well during the last five years. The fund has a longer track record than ICVT (which was created in 2015), so we have to infer quite a bit about how ICVT would have performed during 2008, for example. The Calamos fund was down about 26% compared to the S&P 500’s 37% decline that year. Also, the Calamos fund is actively managed, which makes it more expensive to own than ICVT (1.14% per year vs 0.2%). That extra cost is a drag on performance. ICVT is an index fund and comparing the cost of actively managed funds to index funds is a bit unfair but, just as with the bonds versus stocks comparison, we do it anyway.

Given the complexity of convertibles, I would consider a solid manager with a long-term track record like Calamos, but it’s hard to ignore the relative simplicity and cost savings of index funds like ICVT. Either way, hybrids like convertibles can play a role in the fixed income side of your portfolio if you have room for them. Just be prepared for periods of heightened volatility along the way.

Have questions? Ask me. I can help.

- Created on .