A Quick Look at the Markets

I wanted to take a few minutes this morning to discuss recent market volatility and what, if anything, to do about it. We’ll get back to our list of bond alternatives next week.

For sure these continue to be unsettling times and the list of issues to be concerned about seems only to grow longer. Maybe that’s a little pessimistic, but that’s where my head is at on this Twosday morning.

Anyway, let’s jump right in by reviewing recent performance through last Friday of four popular index funds from Vanguard: Total US Stock Market (VTI), FTSE Developed Markets (VEA), FTSE Emerging Markets (VWO), and Total Bond Market (BND). Together these funds allow for a quick look at how global stocks and US bonds are doing.

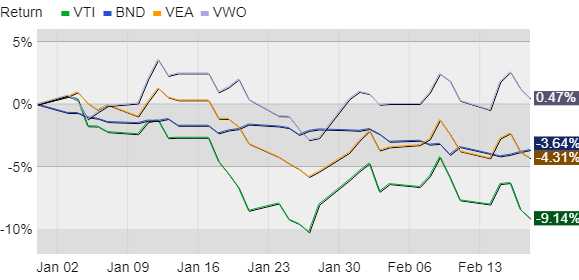

First, year-to-date…

US stocks are down the most, followed by developed foreign stocks (primarily the UK, Europe, and Japan). Perhaps surprisingly, emerging markets (mostly Chinese, Taiwanese, and Indian stocks) have performed well so far this year. These latter two asset classes, and especially emerging markets, have been getting beat up for a while. We have to go back to 2017 to find a time when developed and emerging markets performed better than the US, so there was certainly room for some short-term improvement. And bonds, as we’ve discussed several times in recent weeks, are offering scant comfort lately.

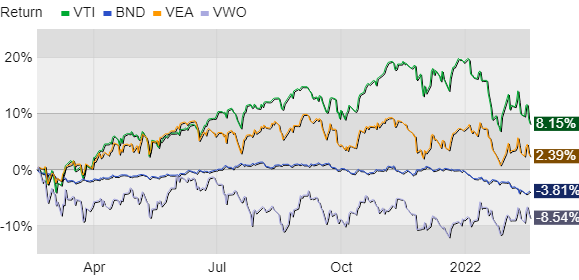

Next let’s stretch out the timeline a bit and look at the last 12 months, again through last Friday…

As 2022 began US stocks, developed foreign, and US bonds all seemed to hit snags at about the same time, and for the same proximate reasons: inflation concerns, how the Fed would/could deal with it, and growing consternation about war in Europe.

Unfortunately, none of those issues are primed for a resolution anytime soon. As we’re all aware, inflation was tracking at 7.5% in January. That’s an average, of course, and the prices of many things we buy regularly are up more than that. The government’s inflation numbers are subject to multiple revisions and may show signs of slowing in the coming months. That’s what the Fed hopes. The markets, however, are assuming inflation will persist and the bond market is currently “pricing in” 4-5 quarter-point rate increases this year. The Fed could raise faster than that, and speculation has been growing for a half-point or even full-point increase at its rate-setting meeting next month. Much will depend on the inflation number for February and any meaningful revisions to prior months.

While inflation and the Fed’s policy response are active and open questions, gauging the outcome of another Russian foreign policy adventure is beyond my ability, and seems to be beyond our government’s ability too. Right or wrong, that adds to the uncertainty of the situation and unsettles investors in what would otherwise be, frankly, a non-event for most of the US economy and our financial markets.

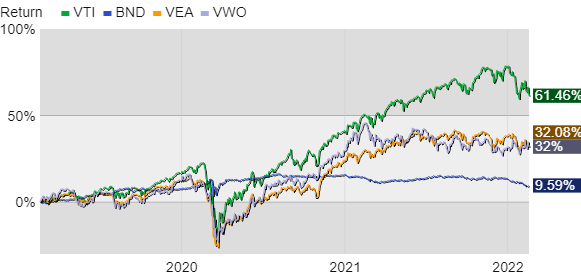

Now let’s broaden our view to the last three years…

These standard asset classes move around a great deal throughout the year and over time. This is totally normal and occurs for a variety of reasons. Even bonds jump around every so often, and we see that in the little blue “W” during the worst of the financial market’s response to the pandemic in March of 2020.

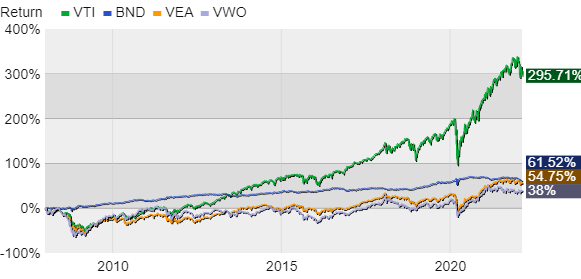

These are arbitrary timeframes but they’re helpful in getting some perspective. To illustrate this point, let’s expand even further and look at performance from January 1st, 2008, a date that captures all four funds (one was created late in 2007). Take a look at the blue bond “W” in 2020 again in this longer-term context. It’s small enough to be a piece of lint on your computer or phone screen. Now add that to the myriad other market (and even cultural) shocks that took place since the Great Financial Crisis. Amid all this volatility, if given enough time the direction remains positive for stocks and bonds as they grow with the economy, each in their own way.

I don’t mention all of this to make light of our current predicament. We have much to be uncertain and concerned about. I hope that inflation moderates over the coming months. While a growing economy needs some inflation, too much too soon is harmful and destabilizes the financial system, even if only for a short while. I also hope that cooler heads prevail in the geopolitical realm. The world has been through much these past two years and a period of relative calm would be welcome by all, or at least by most of us. Fingers crossed.

In any case, as long-term investors we need to be able to weather bouts of uncertainty in hopes of eventually being compensated for our patience. And we will be compensated. If you’re still 10+ years from retirement, stay aggressive if possible. Time is on your side and your regular investments at lower prices will ultimately pay off. If you’re closer to retirement, re-confirm the details of your plan, keep your focus, and adjust as needed. And if you’re one of those who’ve left fulltime work behind, you’ll also want to double check your plan. You’re likely in better shape than you thought.

Beyond that, recent market volatility isn’t that bad. We’ve seen worse but it’s tough to swallow given the emotional roller coaster we’ve been on for almost two years now. To stay on track it’s best to focus on controlling what we can control, like the structure and maintenance of our investment portfolios, while trying (and sometimes failing) not to dwell on the rest.

Have questions? Ask me. I can help.

- Created on .