Commodity Inflation and Other Updates

Inflation, Fed policy, the stock market, the bond market, how Russia’s invasion of Ukraine will continue to impact each one, and the human cost of war. All are on the mind of investors again this week. Oh, and lest we forget our hopeful emergence from the pandemic as well; there’s no rest for the weary.

With all this going on it’s natural for investors to feel nervous, anxious, maybe even panicky. I mean, the word “nuclear” has popped up in different contexts in recent days. The price of oil briefly spiked to $130 per barrel (currently down to $122) and local gas prices are getting ridiculous. And this has been reported in the news with lead-ins like, “Not since 2008 has oil…”. Now, the reporters were likely only referencing the roughly $180 per barrel oil price that year and how it coincided with the Great Financial Crisis, but the connection is enough to make all but the most hardened investors wince.

The GFC was mostly about the structure and incentives of our financial system. Systemic problems and largely unchecked risk-taking allowed millions of consumers to become woefully overburdened by housing debt and led to enormous numbers of defaults. Borrowers were allowed, and even incentivized, to use excessive leverage by big financial companies that were themselves gambling extensively. Then the music stopped and the risk of these too-big-to-fail companies reneging on their agreements to each other caused the system to grind to a halt before almost imploding. Those were white-knuckle times indeed and a reminder of how fragile our modern financial system was and perhaps still is in some ways.

But is the current environment 2008-esque? Russia’s invasion of Ukraine certainly could spiral out of control, directly involve NATO, and lead to more and wider bloodshed. But unless that happens it’s not a structural issue for our economy like the GFC was. Instead, its economic impact seems to be indirect, linked to rising prices for commodities, such as oil and wheat, and how that impacts global demand. Bad timing, of course, because our main issue right now is inflation. But ours was caused in large part by massive amounts of government spending during the pandemic, and Russian aggression/commodity-induced inflation is relatively small when compared to that.

I don’t pretend to know what the future holds, but we can at least check some things off the list of what the current situation isn’t. That said, stock prices could certainly keep grinding lower. (It’s tough to be optimistic with my screens full of red as I write this.) So is it time to throw up our hands, cry uncle, and start looking for advantageous spots in the yard to bury our savings?

Of course my answer is no. I think the best investment strategy is to remain disciplined and focus on rebalancing as our portfolios suggest it’s time to do so, such as buying stocks in modest amounts when they’ve fallen past predetermined thresholds. This has worked throughout all kinds of inclement market weather, and I expect it will continue to do so.

I wanted to share some additional information from JPMorgan and Bespoke again this week (emphasis mine). The former provides us with a look at rising energy prices and the potential impact on American consumers. And the latter provides some updates on the situation in Ukraine.

From JPMorgan…

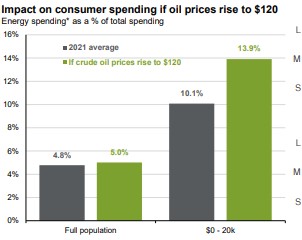

When it comes to economic growth in the United States, the consumer is key, accounting for nearly 70% of gross domestic product (GDP). Following the initial pandemic shock in early 2020, the consumer came back with a vengeance, as stimulus checks and enhanced unemployment benefits stabilized balance sheets across the U.S. and spending on goods accelerated meaningfully. However, with food and energy prices rising, there is a risk that the composition of consumer spending will begin to shift. Looking at energy spending as a percentage of total spending, we are able to model a scenario in which crude oil prices rise to $120 per barrel. In aggregate, however, the model forecasts energy spending would increase to 5.0%, which is only slightly above the 2021 average of 4.8%.

That said, the devil is in the details. To an extent, economic growth has been solid and inflation has been elevated due to stimulus that lined the pockets of lower-income individuals. This group has a much higher marginal propensity to consume – put differently, if they have extra money in their pocket they are more likely to spend than save. As we show in the chart of the week, this cuts both ways. If oil prices spike to $120, energy spending may rise to 13.9% of total spending compared to an average of 10.1% in 2021 for the lowest earning individuals, limiting their ability to consume other items. This could in turn lead to slower economic growth than expected, but also a more rapid decline in core inflation. While we still expect the Federal Reserve (Fed) will hike interest rates at its March meeting, this dynamic may allow the Fed to tighten more gradually than markets currently expect.

From Bespoke Investment Group yesterday morning…

No substantive forward progress has been made by Russian forces in Ukraine since Friday with the exception of a push west towards the Kyiv suburbs on the east side of the Dnieper. It’s not clear whether that lack of progress is due to preparations being made for a new push or if the combination of Ukrainian resistance and Russian logistical ineptitude is driving the slowdown. One significant fact about the fighting over the weekend is that the Russian air force has taken significant losses from Ukrainian surface-to-air missiles and remaining aircraft. The New York Times reported on Sunday that the US alone has already delivered more than 17,000 anti-tank weapons to Ukraine, and that’s only a small slice of the overall military support the country is getting. US intelligence has also reported that Russia has now committed roughly 95% of the forces amassed prior to the invasion, roughly 15% of total military personnel. Outright conquest of Kyiv and most of the country’s landmass is impossible at this point unless something changes significantly. The Russian Ministry of Finance has signaled that it will pay foreign investors in rubles which would ultimately trigger a wave of defaults.

From this morning…

Russian advances remain very slow and deliberate over the last 24 hours. Russian forces are largely consolidating in the south of the country having been pushed out of Mykolaiv (between Crimea an and Odessa) and having made no progress to fully takeover encircled Mariupol. In the northeast, major cities Chernihiv, Surny, and Kharkiv are being bombarded but are not encircled as the advance has stalled out. Slow progress has been made in the west of Kyiv, and Russian forces have advanced from the east in a salient that bypassed Surny. Kyiv is not encircled, and ground lost to Russian forces has been bitterly contested with significant losses imposed by defenders in terms of both material and lives. The Russian military is clearly trying to encircle Kyiv for a siege but has not been able to do so despite progress. Ukrainian units are lighter, more mobile, and are able to avoid large-scale engagements outside of cities, meaning that while Russia has been able to advance, their rear areas are not secure and the supply situation in terms of equipment and consumables is tenuous.

That supply situation is further threatened by the fact that they have not been able to establish air superiority and are vulnerable to strikes from both Turkish-supplied TB2 drones and Ukrainian air force jets. The current situation is therefore a race between the two countries to sap Russian logistics enough that front line troops can no longer hold ground they’ve taken. Despite triumphant social media posts trumpeting Ukrainian success, Russian gains are very real. That said, their logistical situation is dire, morale is unsteady (especially given the loss of at least three generals since the war began, something that almost never happens on modern battlefields), and Ukraine is resisting to a degree that will make outright conquest of the entire country impossible if it continues. We should also note that the US intelligence community now believes Russia has committed all pre-positioned troops and equipment to the fight, meaning that military is getting close to its limits on available manpower.

And some historical perspective, also from Bespoke this morning…

With the entire world focused on the Russia-Ukraine war and possible scenarios under which President Putin can either ratchet up or dial back the tensions, it’s ironic that today marks the 105th anniversary of the start of the ‘February Revolution’ which essentially ended the reign of czarist rule in Russia when Nicholas II abdicated his throne. Historians cite a number of factors for the February Revolution including frustration with government corruption, a poor economy, and autocratic rule, but the Russian military’s poor performance in World War I was the primary catalyst for the Revolution. Russians came out in droves to protest the conditions and despite an attempted crackdown Russian police and ultimately the military, the protestors refused to back down. Within less than a week, Nicholas II abdicated the throne ending the era of czarist rule in the country.

Not long after Nicholas abdicated, Vladamir Lenin returned from exile in Switzerland to lead the Russian Revolution, and as he is often credited with saying, “There are decades where nothing happens, and there are weeks where decades happen.” During the February Revolution, it took less than a week for protests to lead to the abdication of the throne by Nicholas II and usher in the communist era. The current Russia-Ukraine war hasn’t even been two weeks yet, and several years from now, with the benefit of hindsight will we be looking back on this period as another one of those moments where ‘decades’ occurred within a matter of weeks?

Here are links to JPMorgan and Bespoke…

https://www.bespokepremium.com/interactive/

Have questions? Ask me. I can help.

- Created on .