Notes on Rates

Well, last Wednesday was a big day for the markets as the Fed Chair was having his presser to discuss Fed policy and their outlook. Investor mood turned ebullient for a few hours, but the markets have corrected that and then some since. One step up and two steps back. It reminds me of Springsteen and races I’ve run up steep slopes after a hard rain, each step seeming oh-so-futile until, eventually, but I digress…

Since interest rates are all the rage right now, let’s spend a few minutes reviewing where we stand with three rate benchmarks and what’s expected by year-end.

Fed Funds Rate – 0.75% to 1% currently, 2.8% expected

This is the interest rate range at which banks and credit unions lend to themselves to meet reserve requirements, typically via overnight loans. The reserve requirements are set by the Federal Reserve and then the Federal Open Market Committee (a smaller group within the Fed) usually meets eight times a year to set the rate range. Higher rates are meant to slow the flow of money in the system, while the opposite is true for lower rates. “Fed funds”, in a sense, is the axis around which the financial world spins.

Fed funds was lowered to essentially zero during the Great Financial Crisis and the FOMC didn’t start raising it until late-2015. From there the rate was being raised incrementally to about 2.5% as we entered 2020. Then the FOMC again took the rate back to zero when covid hit and it’s taken until now for them to start raising.

Prime Rate – 4% currently, 5.8% expected

We read about the fed funds rate and how it moves markets, yet we’re more impacted by the prime rate day-to-day in the real economy.

Prime is an average interest rate compiled by the Wall Street Journal after surveying our largest banks. It’s thought of as the lowest rate offered by these banks and is typically 3% higher than fed funds. Pre-pandemic, the prime rate was 5.5% since fed funds was at 2.5%. Then it spent many months at 3.25% because the fed funds rate range was 0% - 0.25%. Now we’re back up to 1% for fed funds and a 4% prime rate, that same 3% spread. (I don’t know why it’s a 3% spread, because it doesn’t have to be so far as I’m aware; it just seems generally agreed to in the “modern” era. If you know the history, please enlighten me.)

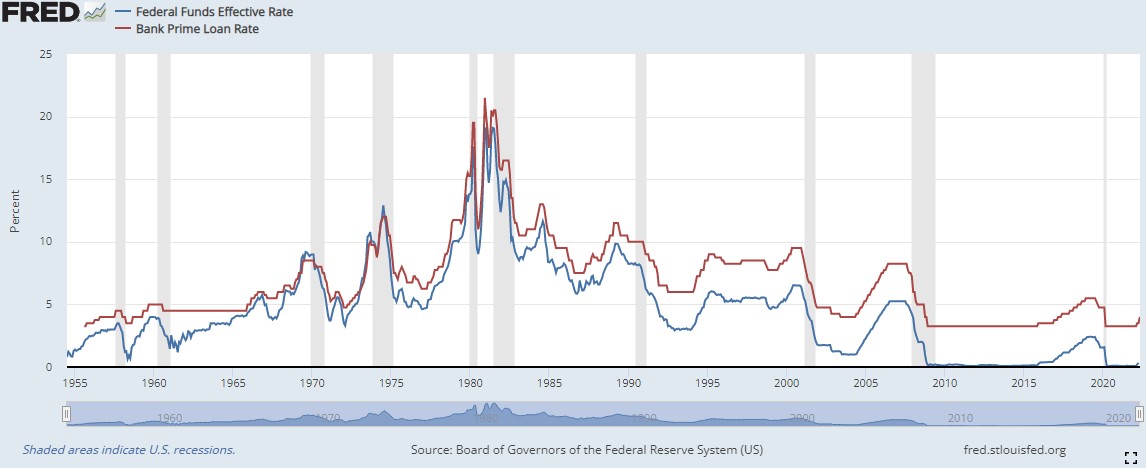

Here's a chart from the St. Louis branch of the Fed that shows the relationship between fed funds and the prime rate over time.

From there it’s all about the spread you pay over prime. Maybe competition makes this smaller for some customers, or maybe a promo rate is less than prime, but currently the direction is higher for all. Investors are expecting the fed funds rate to hit 2.8% by year-end. If so, prime should then be at 5.8% and may continue rising into next year. Still historically low but a big change in a short time.

All this makes new borrowing more expensive than it was even just a few months ago, and impacts auto loans and credit cards, for example. Auto loan rates are about 4.5% nationally, below a pre-pandemic high of about 5%, but still a good deal more than last year. Credit card rates, at least on average, haven’t moved substantially higher yet, but are still north of 16%, according to Bankrate.com.

Prime also impacts some adjustable-rate mortgages and equity lines of credit. There are a variety of so-called reference rates besides prime, but they’re all moving in the same direction. If you have an ARM or a HELOC you should look at your loan paperwork to see what your reference rate is and how often your lender can increase your payment. Most ARMs have a cap for annual increases, which is great since we’re looking at a potential 2+% increase just this year.

10yr Treasury – 3.1% currently and maybe 3.2% expected by year-end (This is driven entirely by markets whereas the prior two benchmarks are set by people at the Fed and big banks.)

Another key benchmark for rates on longer-term loans is the yield on 10yr Treasury securities, wrapped up into something known as the Constant Maturity Treasury. Published by the Fed, the CMT is an average of yields on publicly-traded Treasurys with a 10yr maturity (and it’s published for different timeframes as well). The 10yr CMT doesn’t set mortgage rates but, instead, reflects the market that mortgage bonds have to compete in. Since the overwhelming majority of mortgages are packaged into bonds and sold to investors, the rates paid by borrowers have to keep up.

The 10yr CMT is now just over 3%, following the yield of the 10yr Treasury. That brings the average 30yr fixed mortgage rate to 5.6%, according to the Wall Street Journal, up from 3% or less a year ago. That adds about $122 per month on the principal and interest portion for every $100,000 borrowed. That has to hurt homebuyers who have been diligently bidding on, and often getting outbid on, homes as they watch rates rise in a seller’s market.

So what to make of all this?

Now is a great time to reevaluate your debts. Your fixed-rate mortgage from a purchase or refinance at pretty much any time before this year is going to be in good shape rate-wise. You typically need to save at least half a percent when refinancing to make the costs pencil out, so any rate below 5% is probably locked in at this point.

The same thinking applies to car loans of maybe 4% or below.

Credit cards – you’re not carrying a balance on credit cards are you? If so, and even though average rates on consumer credit haven’t moved a lot higher yet, they’re expected to, so you’ll want to get balances paid off as quickly as possible before that debt gets even more expensive.

Beyond that, and maybe a little bit in the weeds for this post, is to think seriously about taking money out of bonds to buy down (or pay in full) mortgages or other debts with higher interest rates. Longer-term expected returns on core bonds are a little over 3%, so it’s hard to justify borrowing for years at 5+% if you have bonds in non-retirement accounts. This is a facts-and-circumstances sort of thing but is definitely worth considering.

Have questions? Ask me. I can help.

- Created on .