A Few Items to Share

Now that we’ve hit the ground running in the third quarter I wanted to share a few different items with you. First are a couple of surprising stories I read over the weekend. And second is some quick commentary and a chart that will hopefully be reassuring amid all the talk of recession lately.

Now, I’m closer to this sort of information than the average person and I also tend to focus on risk more, but this first article is a reminder of how bad things can get when new financial products come to market faster than the regulators can pay attention.

I’m talking about the rapid rise and dramatic fall of so-called high-yield savings accounts built on the back of digital assets like Bitcoin, Ethereum, and smaller cryptocurrencies. These were all the rage when Bitcoin, for example, was riding high. But as prices fell precipitously so did the shaky foundations that many of these companies were built on.

In this case it’s the bankruptcy filing last week of Voyager, a company that wooed depositors with high interest rates on crypto deposits that could be easily converted into dollars and spent via a debit card. The company’s marketing implied safety and security while being anything but behind closed doors. Ultimately while maybe not a total sham, at a very charitable minimum the company seems to have made light of the variety of risks to depositor’s assets. This led regular people to deposit more and more of their savings, thinking that they were doing the right and responsible thing and, oh yeah, that they were being well-compensated for it along the way.

Did these folks never play the game of musical chairs? Did they not do a basic sniff test to gauge how solid it was to receive high yields on deposits (Voyager touted up to 9% - other companies into the teens) when real banks were offering less than 1%? Nothing is free in this world and financial institutions aren’t in business to give money away. Higher-than-average yields should always smell risky – there has never been a time when this wasn’t true.

There’s absolutely a place for risk in your financial life. We willingly take it with stocks and bonds every day. But we also consciously limit our risk by having a clear line drawn between money that’s investible for long-term growth and what we need to keep safe for shorter-term needs. Blur these lines too much and you’re bound to have problems when markets turn.

I don’t entirely fault the individual depositors referenced in this story. They were enabled by being sold a bill of goods by Voyager and an emerging industry that, I believe, is less concerned with the future of digital assets as a great democratizer of finance than making millions off the backs of unsuspecting and naïve consumers. The game is as old as time. It’s just shocking how easy it still is.

The next article has to do with the average car payment in the US rising to $712 per month. Maybe I’ve been living under a rock but, wow, that seems like a lot of money. And that’s just the average, implying that lots of folks are driving around with a car payment much higher than that. This was originally reported by NPR based on data from Moody’s Analytics.

According to Moody’s, it takes about 41 weeks of a typical person’s income to buy a new vehicle these days, up 14% from a year ago. Supply-chains and inflation are blamed, as is a slew of gadgets and upgrades bringing the average sale price to over $47,000. This seems unsustainable, at least for the typical person, but data from other sources doesn’t show a big uptick in late car payments yet. So long as the economy holds out people should be able to afford these payments.

https://www.npr.org/2022/07/02/1109105779/monthly-car-payments-record-700

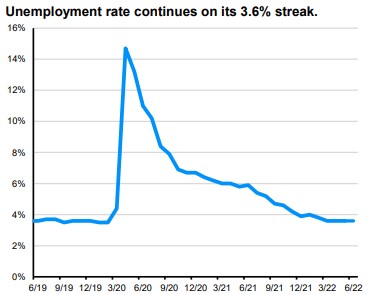

Along those lines, here’s a couple of items from JPMorgan regarding the economy. Ultimately, it’s a mixed bag in terms of positive readings versus others that appear to be rolling over. But a big indicator is the job market, which appears healthy. It’s tough to be in a recession when that’s the case.

Here are some recent thoughts from JPMorgan on the “Are we in a recession?” question:

[…] Recently, recession fears have bubbled to the surface, as the Federal Reserve Bank of Atlanta’s “nowcast” of economic growth now points to a contraction [in this quarter]. This tracker – appropriately named GDPNow – […] suggests that 2Q22 real GDP will decline 2.1% due to a significant slowdown in consumer spending and a contraction in private investment.

[…] Looking ahead, we recognize that recession risk has risen. That said, it seems premature to make a call that we are already in recession today. To start, the labor market remains robust, with job openings still elevated, wage growth solid, and payroll employment growing at a rapid clip. Furthermore, many of the pain points in the economy have begun to correct themselves – commodity prices have come off the boil, inflation looks to have peaked, and market expectations are now for the Federal Reserve to begin cutting rates in 2023.

For investors, it is important to remember that markets are forward looking. Put differently, the equity market tends to peak before a recession starts and trough before the economic data begins to improve. While risks to the outlook have risen, valuations have become more favorable and sentiment is beginning to look washed out; this is not an attempt to call the bottom, but rather a recognition that the outlook for risk assets is more favorable today than was the case at the start of the year.

Have questions? Ask me. I can help.

- Created on .