The Wild Ride Continues

What a crazy year it’s been for the markets! There’s been tons of volatility and the direction most of the time has been southward. Good days have often turned sour, and weeks will go by where it feels like you couldn’t buy a positive day. So it was wild to see just about everything going up dramatically following better-than-expected inflation data coming in last week.

Inflation has been on everyone’s mind this year and, for investors, it’s been all about how the Fed is responding by raising interest rates. With last week’s news of slowing inflation in October following slowing in September from highs in June, the lightning-fast thinking for investors was that the Fed could slow the pace and severity of its rate increases, reducing the risk of creating a recession or making it worse if we’re already dipping our toes into one. More positive data along these lines came in this morning and markets are continuing to respond favorably, at least so far.

Everyone wins if inflation continues to slow, but much remains to be seen in the months ahead. Perhaps ironically, these inflation numbers often get revised so if we end up having seen a major market reaction based on inaccurate numbers it wouldn’t be the first time, positive or negative. But I think in this case it’s less about the specific numbers and more about the changing inflation trend.

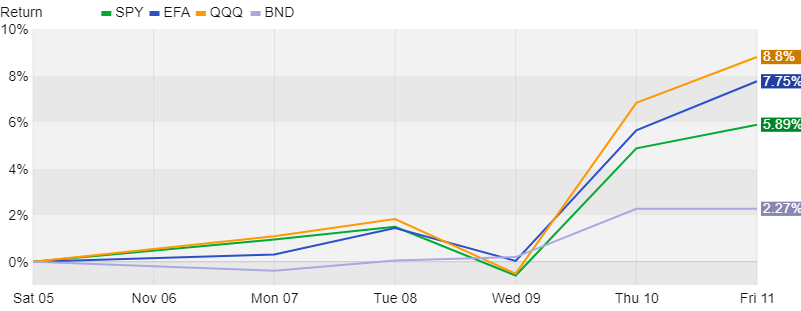

Anyway, I just wanted to share what the market reaction looked like last week. The chart below shows four indexes: the S&P 500 in green, developed foreign stocks in blue, the NASDAQ in orange, and bonds in light blue. It’s easy to see when the news came out! Yes, even after last week stocks are still down 15+% this year and bonds are just a hair better, but it’s still great to see such a positive response to generally positive news.

Among other things, one takeaway from last week’s performance is that it’s impossible to time entry and exists into and out of investments with precision over time. Maybe you get lucky once or even twice. But extend that into investing your serious money and you’re bound to get into trouble.

I’ve picked on the brokerage firm Robinhood in the past and reading what I’m posting below brought them to mind again. The average age of Robinhood clients is 32 and roughly half of its client base are first-timers. Robinhood was/is a proponent of the so-called democratization of finance and, while laudable, is tough to implement. A lot of new investors got sucked in via gamification and faux-free access to markets and rode markets higher before getting beat up this year. According to research by Schwab, many of these younger investors feel a bit chastened and are refocusing for the long-term. If so, this is great because getting the basics right and branching out from there is essential – there are no shortcuts and day trading is perilous at best.

Along these lines, here’s a note from JPMorgan that’s geared toward younger investors but is good information for anyone.

2022 has been a year of remarkable volatility across asset classes. Stocks, bonds and cryptocurrencies have been rocked by a confluence of challenges that could be described as a “perfect storm.” This volatility stems from a number of factors: COVID-19 and its impact on growth in Asia; the war in Ukraine and its impact on global commodity prices; severe economic slowdown thanks in part to a massive fiscal drag; midterm elections, which lead to uncertainty surrounding future policy; multi-decade high inflation; and steadily rising interest rates as global central banks shift policy from accommodative to restrictive.

Asset price volatility impacts all investors regardless of age or income levels. Still, younger investors - namely Millennials and Gen Zers - may struggle more than most. Some of this can be attributed to their relative inexperience in markets, as many had not invested through a bear market; some can be attributed to the lack of guardrails in modern investing, with online brokerage platforms allowing for low- or no-cost access to markets without corresponding advice; and some can be attributed to the composition of younger investors’ portfolios, which heavily favor single securities (like stocks and cryptocurrencies) and options.

Given these circumstances, many younger investors may be wondering how to make sense of current conditions. Broadly speaking, there are three simple steps to better weather volatility:

- Diversify portfolios away from heavily concentrated positions in risky assets. The benefits of the “democratization” of investing in recent years are myriad and it would be imprudent to recommend that young investors liquidate volatile but long-term assets like cryptocurrency. However, it is worth building a well-diversified portfolio around these riskier holdings to mitigate volatility while still embracing risk, which is necessary for young investors given their long-term time horizon, relatively low liquidity needs and poor short-term market prospects.

- Dollar-cost average into markets to avoid market timing pitfalls. Ideally, most young investors are already dollar-cost averaging through regular contributions to 401(k)s. Moreover, these 401(k)s can be “enhanced” by increasing contribution amounts or shifting, if appropriate, into a post-tax “Roth” vehicle. If an investor has reached their contribution limit, investments into non-qualified accounts can be made in the same manner.

- Recognize that heightened volatility is structural in modern markets. Markets, and information more broadly, move faster today than ever. Given the rise of algorithmic trading, high-frequency trading and a more empowered retail investor, this trend will likely accelerate. For this reason, young investors should recognize that future markets will continue to be volatile and become comfortable with this volatility.

All told, younger investors may find today’s volatile market environment uniquely challenging. However, it is possible to manage through these challenges and emerge on the other side with better financial health.

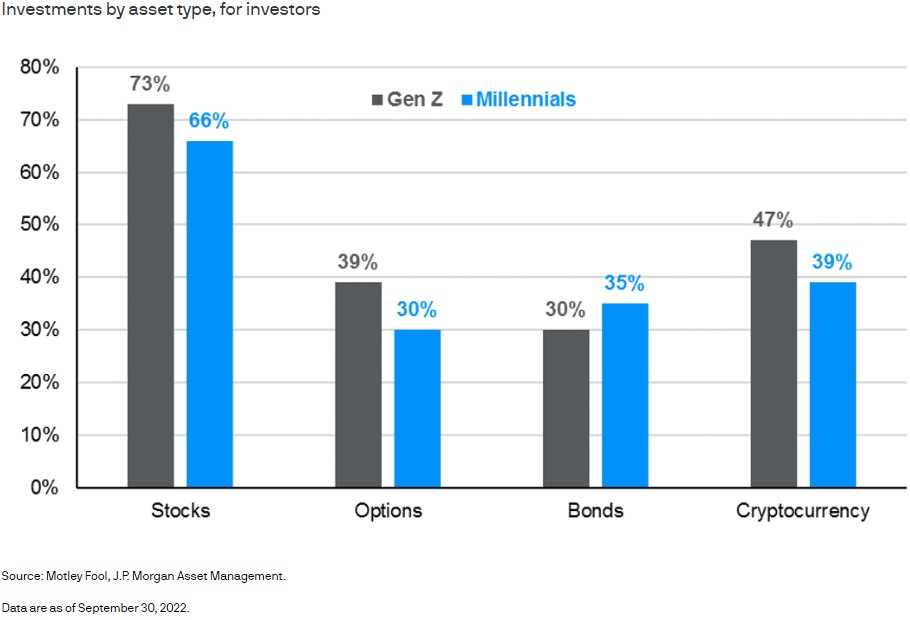

Asset ownership by age group

Here’s a link to JPMorgan’s website if you’d like to read the piece there.

https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/on-the-minds-of-investors/how-can-millennials-ride-out-the-current-market-storm/?email_campaign=304062&email_job=353218&email_contact=003j0000018XcwiAAC&utm_source=clients&utm_medium=email&utm_campaign=ima-mi-publication-wmr-Earnings-11142022&memid=7220927&email_id=65707&decryptFlag=No&e=ZZ&t=613&f=&utm_content=Read-the-latest

Have questions? Ask me. I can help.

- Created on .