Rebalancing and RMDs

It seems like I wonder this every year about now, but how is it almost December? Like it or not we’re almost done with 2022 and there are boxes to check when it comes to our investments. I’m going to quickly offer some notes on two of them, rebalancing and RMDs, with more topics to follow next week.

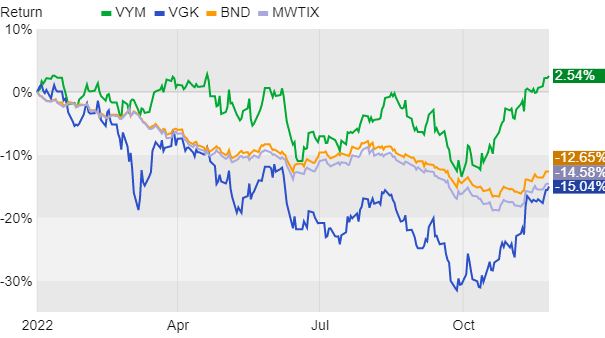

It’s obviously been a rough year for the markets, as you can see from the chart below. Through the holiday-shortened trading day last Friday the stock market as measured by the S&P 500 index (not in the chart) is down about 15%. The Vanguard High Dividend Yield ETF (ticker symbol VYM) and the Vanguard Europe ETF (VGK) are mixed, from up almost 3% to down 16% year-to-date, respectively. You can see below how this performance is better than mere weeks ago, but it still hurts. Bonds are also down year-to-date, and that hurts more in a way, with the Vanguard Total Bond Market ETF (BND) and the Metropolitan West Total Return Fund (MWTIX) down 13% and 15%, respectively.

After 11 months of gyrations you probably need to rebalance your portfolio a bit. And maybe you have an RMD to take because you’re at least age 72 or perhaps have inherited a retirement account. Or maybe you just need to generate some cash for upcoming spending needs. Either way, let’s proceed…

A lot of people wait until year-end to process their RMD. This can be preferable in some cases, but RMDs have to be taken by 12/31 to avoid a penalty. The big brokerage firms are notoriously good at gumming up paperwork for last minute transactions, so the best time to take your RMD is now.

But what should you sell to generate cash in your IRA, 401(k), SEP account, etc? The rebalancing process can help with this question.

I charted the four funds above because they are some of the investments I actually use in client accounts. Each is high quality and I’m not necessarily concerned about this year’s performance – we still want to keep them. But what I’m focused on is rebalancing clients back to their target levels after the recent runup in prices.

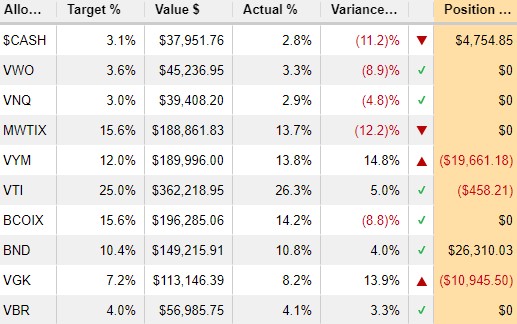

The chart below shows holdings in a real account and their size relative to the target weighting I set. You’ll see that VYM has a target weighting of 12% but a current weighting of almost 14%, about 15% above target. VGK is up about 14% relative to its target. Conversely, the bond fund MWTIX is down 12% relative to target while BND is pretty flat.

Ordinarily I’d let VYM and VGK float a bit longer, perhaps up to a 20% variance, before doing anything. However, this client has an upcoming RMD and there’s room to cut, so we’ll trim back stocks and send money to the client’s bank account. I’ll then add remaining sale proceeds to bonds, most likely MWTIX since it’s lowest relative to target. Of course we could sell MWTIX instead of stocks because it’s already down and there must be something wrong with it. But that would create more of an imbalance in the client’s portfolio and, as I already indicated, there’s nothing wrong with the fund – it’s just down with the market.

Rebalancing like this helps ensure the components of our portfolios are allowed to move with market conditions, but not get too out of whack along the way. I do this throughout the year for clients but if you’re only doing this once, year-end seems like a good time.

Ideally you’d follow a process where each investment in your portfolio has a target to compare to. This requires data and tech to evaluate the data, something often challenging for a retail investor. Instead, you could look at a chart similar to the one I’ve posted above and generate cash from the best performers, not the worst. This year that’s probably dividend-oriented funds such as VYM or shorter-term bond funds that are down less than typical. Or maybe it’s from funds like VGK that have runup faster lately. Do the best with what data you have and remember to ask questions.

Also, the IRS doesn’t necessarily care what you do with your RMD – just that it leaves your retirement account and becomes taxable. This means you can punt any rebalancing decisions by moving shares of one or more investments from your retirement account into a non-retirement account. This might seem like a simple solution, but I definitely wouldn’t surprise your brokerage firm with this request too late in the year.

Another also: Remember that beginning at age 70.5 (the actual month and not earlier) you can gift directly to charity from your retirement account. This age limit is a holdover from when RMDs began at 70.5 instead of the current starting age of 72. Either way, you can direct your brokerage firm (or your humble financial planner) to have checks sent directly to charities from your account, up to $100,000 per year with no minimum. You won’t get to deduct the charitable contribution, but you won’t have to declare the distribution as income either. If you’re planning to make charitable gifts anyway and are required to take an RMD, Qualified Charitable Distributions are often the better option taxwise.

Have questions? Ask me. I can help.

- Created on .