A Kinder, Gentler Fed?

Wondering why your investments have been performing better lately? While I’d love to take the credit, the turnabout for stocks and bonds so far this year is, as always, due to a variety of factors. But the most important factor is still Federal Reserve policy. The Fed, and concerns about how its interest rate decisions would be implemented, dominated the conversation last year and helped send markets down often in the teens or more than 20%, depending on which index you look at. We’re still hyper focused on the Fed, but the rhetoric has changed a bit and so has the mood.

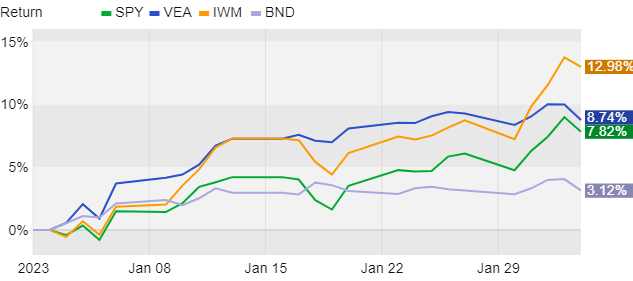

So far this year we’ve seen a marked difference in performance from last year. The S&P 500 is up almost 8% through last Friday, foreign stocks are up nearly 9%, small caps up 13%, and even bonds, the real disappointment last year, are up 3%. Check out the chart below. The green line is the S&P 500, blue is foreign stocks, orange is small caps, and bonds get to be lavender this week.

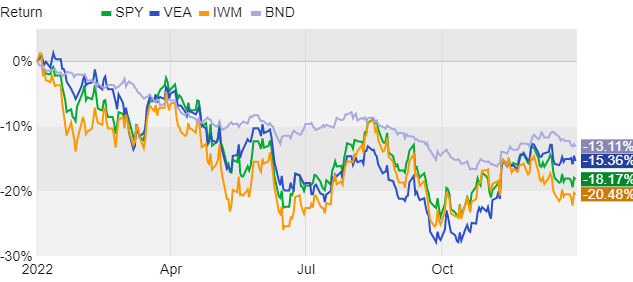

It’s still early days yet for 2023, but this is obviously a welcome sight over last year, even if short-lived. As a reminder, here’s what last year looked like for the same indexes.

So what gives? Investors are still wondering and worrying about inflation, the likelihood of recession, and how Fed policy could impact it all. If the Fed keeps raising rates too much too quickly a recession is likely because money costs a lot more to borrow, and that gums up the system. For example, the Prime Rate, a key consumer finance benchmark, was 3.25% a year ago but is now 7.75%. This impacts the cost of credit card balances and HELOCs, among other things, and when it’s high consumer spending is sure to slow, perhaps quickly. But if the Fed turns kinder and gentler and takes more of a wait-and-see approach, consumption could stay strong, corporate profits remain relatively high, and maybe we’d avoid a recession. That’s the thinking anyway. As all this unfolds market participants scrutinize everything coming out of the Fed, looking for clues about which Fed we’ll be dealing with. This makes the Fed’s interest rate decisions and, perhaps more importantly, how the information is delivered by the Fed Chair incredibly important – the words and tone used, the body language, all of it impacts markets.

That might sound a little farfetched but it’s true. For years the Fed chairperson has held a live press conference following the announcement of its interest rate decisions. Prior to this it was just a press release without much accompanying color. These press conferences offer the media a regular formal opportunity to ask questions about the economy, if the Fed felt growth was too hot or too cold, and what it was planning to do about it. As you can imagine, these pressers could sometimes be a snooze fest, only interesting to people who really pay attention. But other times, such as during the pandemic’s early days and over recent months as inflation was catching everyone off guard, watching the Q&A felt like living history and markets often responded negatively, but sometimes positive in a big way.

Such was the case last week when Fed Chair Jerome Powell took to the lectern to deliver his remarks and take questions from the financial press. Inflation is still too high but has been waning, he said, using the term “disinflation” several times. He described how the tough work they’ve done by raising rates so much has been working without causing too much havoc in the economy. The job market is strong with unemployment at 3.4%, a historic low, with nearly two jobs available or every job seeker. Risk of recession is still present, but there’s a decent chance the economy avoids recession, or at least a major one, as inflation gets back to acceptable levels. And Chair Powell elaborated more than usual on how a so-called soft landing could play out and peeled the layers back further on some of the metrics he uses to keep tabs on the economy.

Ultimately the Fed opted to raise short-term rates by 0.25% instead of 0.5%, as had been become normalized in recent months. This smaller increase, coupled with Chair Powell’s relatively upbeat remarks, was cheered by markets. Only time will tell, of course, if we can get out of this situation relatively unscathed, but here’s hoping for the best-case scenario!

While you don’t have to watch these press conferences regularly, consider watching last week’s. Powell doesn’t make investment recommendations or try to sell a narrative. Instead, it’s about 45 mins of how, arguably, the most important person in the financial markets right now feels about inflation, our economy, and the outlook. All important context, straight from the source.

Here’s a link to the Fed’s homepage. The video plays right from the home screen.

https://www.federalreserve.gov/

As an aside, I just finished some intro stuff about ChatGPT and feel compelled to offer that I personally wrote everything above, for better or worse. One quality peice I read about this new tech floored me a bit when I got to the end and was informed that ChatGPT had written about 2/3rds of the article. And then separately my research folks used today as the 59th anniversary of the Beatles landing to suggest that ChatGPT is as much of a societal gamechanger as the boys from Liverpool. Quite the statement! If you haven't already, take a few minutes to check this out. Here's one of very many videos on the topic.

https://www.youtube.com/watch?v=Pm34OBs9W_g

Have questions? Ask us. We can help.

- Created on .