A Few Quick Updates

There’s truly never a dull moment, whether in life or in the financial markets. As we look ahead to summer there’s a short but weighty list of issues to follow: the debt ceiling, the banking “crisis”, the Fed, interest rates and recession risk. All this is playing out at the same time and demands our attention.

You’ve likely been wondering about these issues and many of you have been asking, so here are some thoughts pertaining to each.

The debt ceiling debate –

Treasury Secretary Janet Yellen recently said that Congress not raising our government’s borrowing limit would be a “catastrophe". I doubt she used that word lightly. As we’ve discussed previously, our debt ceiling is an arbitrary dollar amount that Congress has for years typically raised or suspended for a time. It’s been this way for over 100 years since the debt limit was created and, at least in modern times, has usually been subject to vigorous and often nerve-racking debate. This makes sense, of course, because all this deals with how much we borrow and that’s a sensitive topic for most people. (Even though the federal government isn’t a household and prudent borrowing standards we teach to our kids don’t necessarily apply, but I digress…)

So, while experts tend to agree that Congress failing to raise the debt limit, leading to missed payments and a technical default by the US Treasury, is not likely to actually happen, the same experts all expect political brinksmanship to take us down to the wire again. This is important as we’re nearing the so-called X Date when current “extraordinary measures to fund the government” dry up because the debt limit needs to be raised, not because we’re actually out of money. Our government can easily borrow more from domestic and global markets at any time.

President Biden and a variety of others are meeting on this later today. Both sides agree that the debt limit should be raised but fundamentally disagree on the means of raising it. That sounds about like a game of chicken where both sides agree they shouldn’t hit each other but neither is willing to veer away. Again, never a dull moment.

But how are the markets likely to respond? Here’s a good piece in this vein from PIMCO, the noted fund manager.

And here’s a recent press release from the Treasury department regarding this issue. There’s no shortage of cash and access to more, we just lack Congress’s permission to keep the wheels in motion.

https://home.treasury.gov/news/press-releases/jy1460

The banking crisis –

I put the word crisis in quotes earlier because the problem’s depth is a matter of perspective. An interesting take on this comes from Gallup. The polling company recently measured how worried Americans are about the banking sector and the results were about the same as during the Great Financial Crisis, even though we’re not in the midst of that, thank heavens. And the poll was conducted last month before First Republic got swallowed up by JPMorgan!

We’re used to thinking of banks as solid and safe, even boring institutions, so it’s interesting to see how worried we tend to get about them. More educated and affluent Americans are less worried though, as are Democrats. This is flipped around from the GFC and presumably has something to do with who’s in the White House at the time. For example, in 2008, 55% of Democrats were “very or moderately worried” about banks, but as of last month Republicans held that same percentage spot.

Here’s the Gallup article.

https://news.gallup.com/poll/505439/half-worry-money-safety-banks.aspx

Whatever the reasons and political affiliations, people are concerned about how safe their cash is. This is entirely reasonable given all the news and hyperbole about the financial system lately. We’re all now probably well aware of the basics of FDIC and NCUA insurance, so I won’t bore you with that again here, but please ask if you have questions.

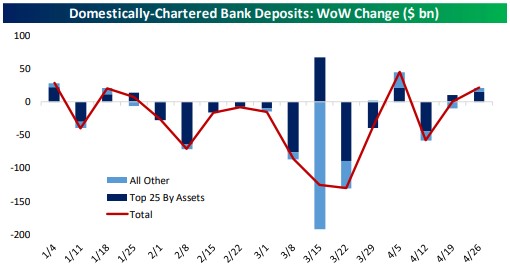

Instead, it’s news this week that the banking system has been functioning much better after several weeks of uncertainty. According to my research partners at Bespoke Investment Group, banks are lending to each other again and deposits are on the rise, both for the top 25 banks by assets and smaller banks as well. This is good news after the huge drop in deposits at regional banks in mid- to late-March. Loans are also on the rise, especially at the smaller banks.

That said, I’d be surprised if there wasn’t news in the coming weeks of other smaller banks getting absorbed by their larger brethren. Just be prepared for that news and try to keep your balances within federal insurance limits just in case. It’s the prudent thing to do even though risk is low.

Interest rates and recession risk –

The Fed raised rates again last week by another 0.25%, bringing its benchmark rate to 5.25%. Markets are expecting that this will be the last rate bump for awhile and even that rates could start going down later this year. Why would they go down after going up so much in recent months? Recession.

This might take longer to materialize than some analysts were expecting even weeks ago. Unemployment is incredibly low, and wages are up while slowing consistently from a high point a year ago. Housing remains strong across much of the country and the consumer is still out there buying. Inflation is still high while coming down steadily. But employers are reporting fewer job openings and they seem to be prepping for a slowdown. There’s also an assumption that recent banking issues will put a dent in lending and demand, although that hasn’t shown up clearly in the numbers yet. That’s an example of the mix of economic data coming out lately, but the overall trend seems to be softening.

So that’s where we’re at right now and mixing it all together seems to indicate a banking sector that’s dodged a bullet, and a strong economy losing momentum that, in a perfect world, would only need to dip its toe into a recession. The 800-pound gorilla in the room is the debt ceiling debate and potential default, so let’s hope that cooler heads prevail in those fancy meeting rooms in DC.

Have questions? Ask us. We can help.

- Created on .