The SpaceX IPO caused a lot of excitement and consternation last week, and neither is expected to die down anytime soon. The excitement part is pretty easy to explain; it’s about money or perhaps opportunity. The consternation part is more complicated.

While I try to keep my opinions about any company founder or CEO as professional as possible, I understand how Elon Musk drives a lot of people crazy. There are various reasons why, so I’ll let you recall your own. This matters with SpaceX because, as I understand it, Mr. Musk personally controls over 80% of the voting power at the company and, presumably and consequently, won’t have to worry very much about what his stockholders think. This is in contrast to Tesla, for which he holds something like 20% of the vote. So, SpaceX is really all about Elon Musk and, while that’s exciting for a lot of investors, others are concerned about how SpaceX’s inclusion into major stock market indices might inject this polarizing figure further into their portfolio.

As I type, SpaceX is valued at around $2.5 trillion by the stock market and overnight briefly surpassed Microsoft in market capitalization before falling to around Amazon’s value.

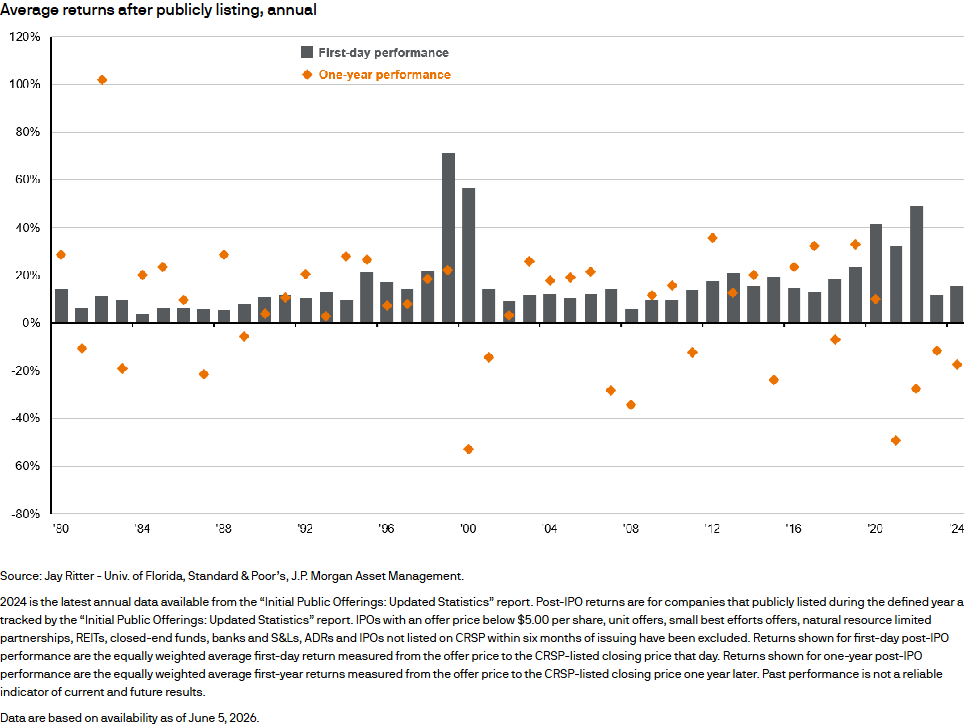

Frankly, that seems a little ridiculous but will that last? The chart below shows how IPOs can quickly lose favor, especially once insiders are able to sell their shares, so only time will tell what SpaceX’s fair value is. Regarding stock indexes, the NASDAQ, MSCI, and other providers are “fast-tracking” SpaceX’s inclusion into their indexes, while the S&P 500 is not. All this will be instructive for other mega-IPOs that are expected to come to market later this year.

Along these lines, here’s a piece from JP Morgan about what index providers are doing, or not doing in some cases, to alter their portfolios to account for SpaceX.

As a reminder, I have software that can tell us how much exposure we have to a specific company within a portfolio of funds. This provides useful information on several levels and lets us emphasize or reduce exposure accordingly. So once SpaceX starts popping up in the indexes, we’ll be able to see exactly how much exposure you have to it and, if necessary, discuss what to do about it.

From JP Morgan…

Some rebalancing activity is to be expected, which could translate into short-term volatility.

There are now more than 800 venture-backed private companies valued at over $1 billion, and a handful of private companies that have raised capital at valuations near $1 trillion. When these companies eventually IPO, they could become meaningful components of public stock indices and ordinary investors’ portfolios.

How big a splash could large IPOs make when they first begin trading?

An important point to keep in mind for initial public offerings is that they typically float only a small fraction of the total shares, rather than releasing them all in one go. That helps to facilitate an orderly entry into the trading flow, allowing markets to digest the volume gradually. A large chunk of shares owned by private owners can remain locked up for 6 months or longer.

That means that a trillion-dollar IPO isn’t automatically a trillion-dollar market event on day one, and the impact on markets can be managed to limit volatility.

When will large IPOs be included in stock indices?

Stock indices are rewriting their rules to adapt to the new phenomenon of mega-cap IPOs. The index providers behind the Nasdaq 100 and the Russell 1000 indices have released commentary around how they would “fast track” the inclusion of large companies in their indices. Based on these announcements, mega-cap companies could join the indices in a matter of weeks or months, rather than taking years as is typically the case with IPOs of smaller companies. The index provider behind the S&P 500 index opted to keep its current inclusion rules in place, which includes at least a 12-month seasoning period as a public company, financial profitability and a minimum 10% of its shares available to the public.

The weighting of companies in indices is typically based on the free float, or the percentage of shares available to public investors. So during initial trading, with a free float of 5% for example, a company that is a mega-cap in terms of total valuation might still make up a relatively small percentage of the index. Some index providers have chosen to apply multipliers to the free float percentage of new IPOs, which could amplify their impact on the index.

Will funds have to sell some stocks to buy new ones?

Not necessarily. Funds that have strong inflows can use capital to preferentially acquire newly minted shares without having to sell existing holdings. And managers have some flexibility to manage liquidity in advance so they are able to deploy it into new listings.

That said, some rebalancing activity is to be expected, which could translate into short-term volatility. Strategies that are actively managed and can allow small deviations from passive benchmarks may be able to better manage volatility and take advantage of timing opportunities than passive strategies.

How will index composition adapt over time?

As more shares are floated, and as lock-up periods expire, the weights of new companies in the indices will grow. The performance of the companies post-IPO, and therefore their valuation, will also determine their ultimate weight in stock indices.

What to expect in early trading?

Freshly floated stocks can be volatile, as investors process new information and form opinions on valuation. The average IPO this decade, for example, popped 32% on the first day of trading, but was down 26% from its offering price after one year. Headlines at the bell-ringing event can create early excitement, but ultimately the fundamentals of company performance determines where stock prices land after the confetti settles.

First-day and one-year post-IPO stock performance

Have questions? Ask us. We can help.