The last handful of days has seen a new Fed Chair, the death of a former Chair, and the demise of yet another UK Prime Minister. That’s a few out of many recent headlines that also include the on-again-off-again peace process with Iran, but let’s review the first three this morning.

At the Fed, Kevin Warsh had his first Fed rate-setting meeting and press conference last week. He was comparatively brief and direct in his delivery style. Among other things, Warsh told markets to expect some changes to the way things are done at the Fed (following the work of various task forces he is creating), but that its core missions of ensuring price stability and full employment would remain the focus. Specifically, Warsh hammered home how the Fed would get inflation under control.

It’s interesting to watch how markets respond as the Fed Chair delivers prepared remarks and answers questions from reporters during the post-meeting press conference. The presser is common now, but Fed Chairs didn’t use to have to do that, or at least not as often. Markets hung in there with him until the last 30 or so minutes of trading before the major indexes ultimately dropped over a percent for the day. One day does not make a trend, but markets are coming to grips with interest rates that are now expected to rise instead of fall. We’ve talked about this in recent weeks so it’s not new information, but perhaps some traders were hoping for a surprisingly “dovish” speech from the new Fed Chair. They didn’t get it.

Coincidentally, we lost former Fed Chair Alan Greenspan over the weekend to complications from Parkinson’s disease at age 100. The “Maestro” served as Chair for nearly 19 years under four presidents and oversaw (if that’s the right word) one of the longest economic expansions in US history. Unfortunately, and with the benefit of hindsight, many now point to Greenspan’s policies as contributing to the real estate bubble and subsequent Great Recession that followed his retirement as Chair in 2006. Numerous obituaries are out there, including the link below from The Wall Street Journal, so I won’t get into all that here. Still, serving as Fed Chair is a tough and consequential job that Alan Greenspan performed longer than most, so for that I tip my hat to him, regardless of what some market historians might say.

Another tough job, especially during these days of zero patience and a short attention span, is that of UK Prime Minister. Keir Starmer was elected in a landslide a couple of years ago but struggled right off the bat and echoed the plight of recent prime ministers (six in the last seven years, including Liz Truss for just seven weeks in 2022). Starmer just resigned after two years in office and will serve in a caretaker role until a new Prime Minister can be elected. Ironically, the Brexit referendum that started this volatile period in British politics was ten years ago today. And the same forces that led to Brexit are still at play, perhaps explaining why the political environment is so tenuous.

There aren’t many direct investment implications for US investors related to the UK’s prime minister issues beyond how political instability abroad keeps uncertainty high for everybody. That’s unlikely to change anytime soon and not just in Great Brittain. Along these lines, here are portions of some interesting commentary and a chart from my research partners at Bespoke Investment Group.

The UK’s political system has claimed another Prime Minister [… yesterday] morning Labour’s leader Kier Starmer announced he would step down. His departure was widely expected after Manchester mayor Andy Burnham won a by-election in the suburbs of that city last week in convincing fashion. While Starmer has suffered a similar popularity decline to the string of Tory PMs that followed the resignation of David Cameron following the Brexit vote in 2016, it wasn’t clear who could garner broad support from across the Labour Party to replace him as leader until Burnham was proposed as an alternative. Burnham wasn’t an MP, so another Labour MP stepped down to give him the seat he then won. [As I understand it, at this point there are no challengers, so Mr. Burnham seems likely to be Starmer’s replacement.]

The UK political system is very much designed to handle these sorts of rapid leadership changes; the failure of Starmer to last more than a couple of years is not a crisis in any immediate sense.

Parliamentary elections are due no later than August of 2029, so the change at the top of the Labour Party does not mean voters will be called to the polls. The UK also has a much smaller political executive than the US thanks to their executive being derived from elected representatives.

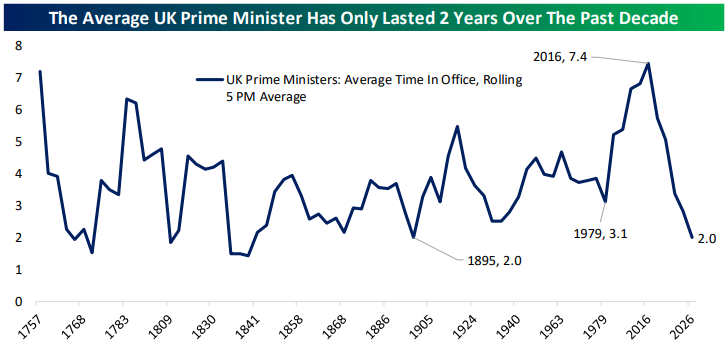

That said we do think there is an interesting message in the data around average Prime Ministerial tenure. Back to the early 18th century, the average term has been 3.8 years, though that’s skewed higher by outliers (median 2.6 years). As shown in the chart below left, Cameron’s resignation ended a period of rapidly increasing tenure that peaked with his. At 7.4 years, the period ended 2016 was the longest five-PM average tenure on record.

Incidentally, that period covered Prime Ministers whose tenures ended between 1990 and 2016, starting with Margaret Thatcher (11.6 years) and including Tony Blair (10.2 years). If we think of Prime Minister tenure as a proxy for overall political stability, the 1990s and 2000s were incredibly stable. Obviously, this is only the UK, but the post-Cold War environment across the developed world broadly reflected the same trends of few big fights over ideology and broad national consensus over basic policy.

It’s no coincidence, in our view, that the result was a decline in inflation, interest rates, and stock market risk premiums. Again, that dynamic is not UK-specific; we just think the chart [above] does a very good job of delineating the period of the “end of history” period and the political world developed countries now occupy. 2.0 years is the shortest 5-PM average tenure for the UK since the 19th century and excluding that joint-same period the lowest since before the US Civil War. We live in a period of increasing political and therefore policy volatility, with realignments of traditional voting coalitions and a much broader range of possible consensus or median voter preference than existed over the last three decades.

Have questions? Ask us. We can help.