How many times have I started these posts this year with something along the lines of “It’s rough out there for investors…”? Doing so often leaves me feeling like Captain Obvious but, as they say, it is what it is.

This week I’ll jump right in because I want to share a variety of information about what’s happening in the markets.

September is typically one of the worst months of the year for investors, so a few more days and then it’s good riddance as we enter the fourth quarter, usually the best time of year for investors. We’ll see. So far in 2022 major stock indexes are down from 18% to 30%, so Mr. Market has his work cut out.

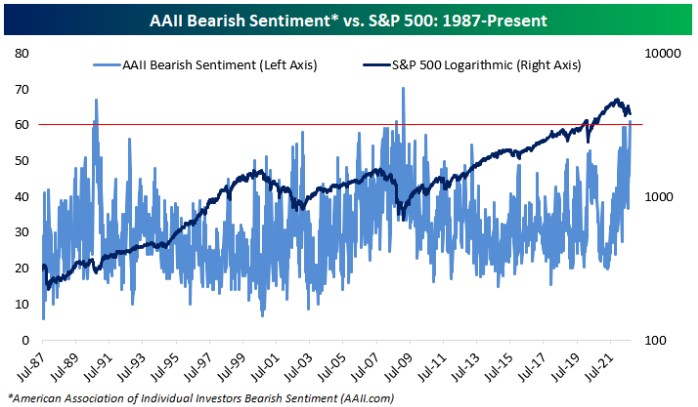

News from the past week shows us what we already know: the market’s mood is nasty right now and the few positive catalysts tend to be drowned out by negative noise. That shows up in market breadth (stocks advancing vs declining, currently the lowest it’s been in decades), volatility levels, and investor sentiment surveys. Sentiment is a known contrarian indicator, albeit an imperfect one.

This chart from Bespoke Investment Group shows the American Association of Individual Investors sentiment survey over recent decades. You’ll see via the red line that we’re at the level of extreme investor bearishness. News like this should make the contrarian’s ears perk up because, as the Warren Buffet quote goes, we should buy when others are fearful. But the timing on this isn’t perfect. The next chart uses the Great Financial Crisis to show that extreme bearishness can begat more extreme bearishness in the short-term before the market finally turns positive.

The good news is that from a historical perspective, from this point on and even more so should sentiment worsen from here, return expectations for the year ahead and beyond only get better.

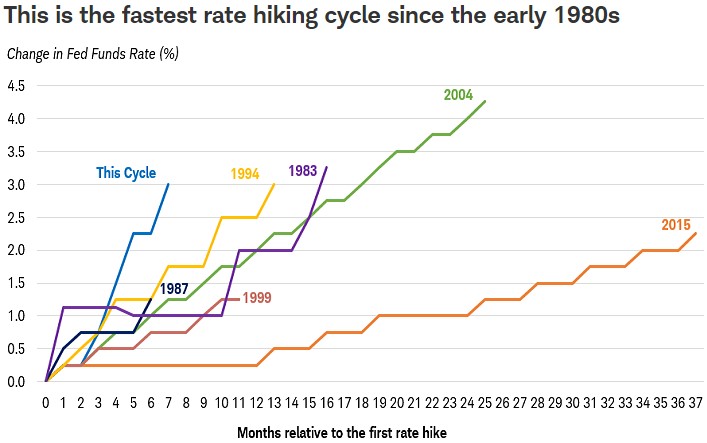

What could make sentiment get worse? The Fed. They raised rates again by 0.75% last week for a total of 3% this year. A major problem with this is, even as Fed Chair Jerome Powell has reiterated in recent days, rate increases “have a long and variable lag”, meaning that even one increase can take months to play out across the economy. And we’ve had five since March with more expected. There’s a growing risk that the Fed has pushed too far too fast, setting the stage for unanticipated consequences within the economy. Also in recent days members of the Fed, including the Chair, have doubled down on their willingness to allow people in the economy to go through “pain” while trying to avoid “deep, deep pain” (whatever that means) as the Fed fights inflation. It’s reasonable if statements like those don’t inspire a lot of confidence.

This next chart from JP Morgan provides some historical context for Fed hiking cycles and it’s easy to see the quickness of this one. As the Fed lowers rates they’re said to be spiking the punchbowl. If you’ll pardon the analogy, these rate increases could be like walking into the party and doing five tequila shots at the door. Maybe you’d be okay if you spaced your shots throughout the night. But slam five back-to-back and you’re asking for a long night and a hangover.

The rapid pace of rate hikes coupled with evolving rhetoric from the Fed have roiled the bond markets this year. And comments like, “Nobody knows whether this process will lead to a recession,” coming from the Fed Chair last week don’t help, even though he sounded reasonable and truthful (would investors rather he lied?). Nonetheless, it freaked investors out. The Bloomberg Barclays Bond Index, sort of like the S&P 500 for the bond market, declined a bit further and is down almost 14% this year, something very rare for bonds.

These gyrations have led to inversions within the yield curve, an important indicator that we’ve discussed before. These inversions steepened last week.

For example, as I write you can buy a US Treasury maturing in two years and earn an annual rate of 4.26%. If you bought a 10yr bond you’d earn 3.85%. That lower yield on a longer bond (the inversion) doesn’t ordinarily exist and is said to be a strong indicator of a looming recession. And for many investors the difference being relatively large cements recession expectations.

NPR had a good article (with audio, about 4 minutes) discussing the bond market this year. Give it a listen for a straightforward reminder of how bonds work and why, even amid all the chaos, they’re still good to own.

https://www.npr.org/2022/09/25/1124838564/stocks-and-bonds-both-get-clobbered-this-time-heres-whats-behind-the-double-wham

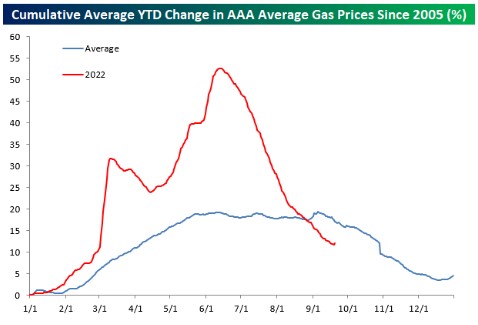

Consumers are facing challenges but it’s not all bad. Inflation is high but some prices, such as for gasoline, have been falling. Last week the AAA national average price for gas ended its especially long run of 98 days of declines. This next chart from Bespoke shows what a wild ride it’s been for gas prices this year.

Gasoline is a relatively small component of the CPI inflation measure, but it’s psychologically important for consumers, with lower prices usually being a boon for confidence. But not lately. Maybe that’s because compared to last year gas prices are still about 26% higher and housing costs, a larger portion of CPI, are up with no near-term signs of slowing. On the positive side, consumers and investors are holding a large amount of cash measured in the trillions. This lessens the impact of inflation for most people and provides money to invest when, and not if, sentiment finally turns positive.

So what are you supposed to do with your investments in this sort of environment? In all seriousness, hang on for dear life. We’ve been through a lot of rockiness and there may still be more to come. Your investments have been taking a beating, but their prices will recover.

Remember that the thousands of stocks represented in your diversified portfolio are actual companies that are still in business. They were today and they will be tomorrow. And the bonds are issued by entities like the US Treasury, high-quality corporations, and perhaps states and municipalities. The vast majority of these bond issuers will continue to pay interest on schedule. The share price of the stocks and bonds has fallen, mostly because it’s too hard to price them amid all the uncertainty, but their fundamental, long-term value remains.

Focus on structural issues like investment quality, cost, and rebalancing. The latter has been challenging this year for a variety of reasons, but the process still works and the discipline still adds value.

The other thing to do: Ask questions. Don’t let them fester. You’re likely in better financial shape than you realize, or than it seems from watching the news, so try not to let anxiety get the better of you.

Here are a couple links to Bespoke’s work if you’d like to check out their research.

https://www.bespokepremium.com/interactive/posts/think-big-blog/the-streak-is-over

https://www.bespokepremium.com/interactive/posts/chart-of-the-day/chart-of-the-day-bearish-sentiment-soars-but-might-not-have-peaked

Have questions? Ask me. I can help.