Bonds or What Else?

At about this time each year I go through a due dilligence process to review investments that I use in client portfolios. I look at quality, cost, performance, compare to alternatives, and try to poke some holes in my logic about using Fund A versus Fund B, and so forth. Of course I’m biased because I liked the investments enough to use them in the first place, but I try hard to be objective. All this work usually leads to few changes. Instead, it’s often a recommittment to using what we already own.

That said, a real struggle right now is what to do about bonds. The asset class, as we’re all aware, has been underperforming for awhile and headwinds are building. The Fed is expected to raise short-term interest rates three or more times this year to fend off the inflation monster. The mixed messages in the economy right now, such as headfakes coming from the labor market (very low unemployment of 3.9% but very high amounts of job openings amid the so-called Great Resignation) have got to be confusing for Fed policymakers. And this isn’t helping the confidence of bond investors.

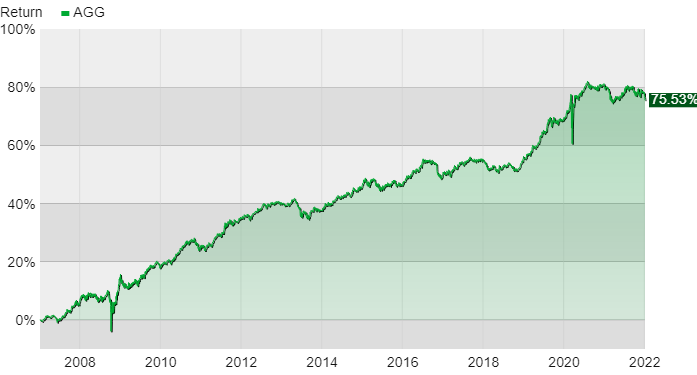

Core bonds lost nearly two percent last year and have taken another leg down of about 1.5% (as of yesterday) to start 2022. While dishesartening, it’s important to remember that the bond market isn’t immune from volatility. Looking back at performance for a common bond index fund since 2008 we see a steady rise in value with several bouts of nastiness along the way. The two big ones were during the Great Financial Crisis and then again recently during the early days of the pandemic. Of course, this is nothing like stock market volatility but it’s still unsettling for investors when even this “safe” asset class gets wobbly.

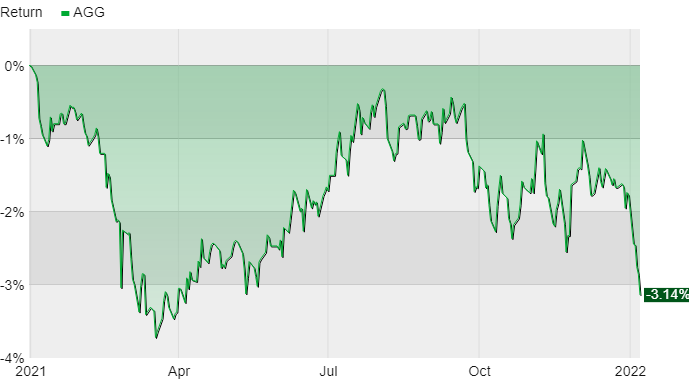

But looking at more recent performance of the same fund, we see a bond market continuing to digest lots of uncertainty. The chart below looks like a rollercoaster ride but if we compared the fund to the stock market you’d see how relatively mellow bonds were, even though they finshed last year and through yesterday lower.

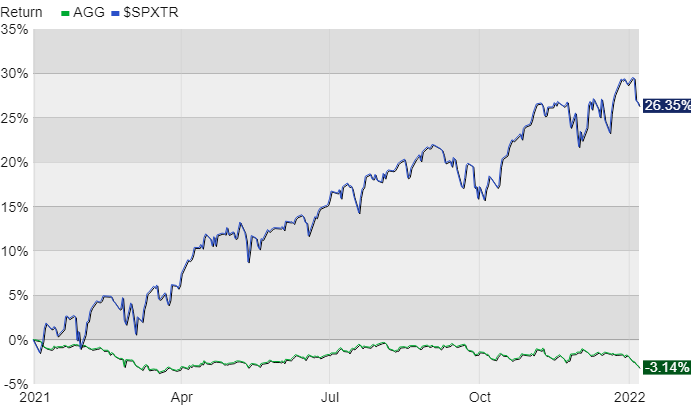

Here’s the chart adding stocks over the same timeframe.

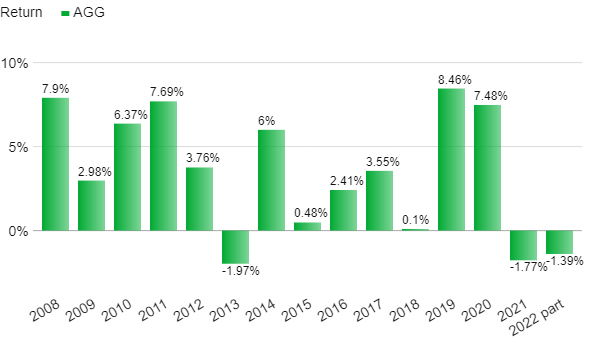

To illustrate the reversal, or perhaps the stalling of bonds lately, this final chart shows year-by-year performance going back to 2008. Low and declining interest rates were the main driver over this timeframe. We don’t know how many times the Fed will actually raise rates this year and if this will begin a fundamental shift to a rising rate envronment. Market prognosticators have been expecting this for years now and, for lots of reasons, it hasn’t happened. Still, it’s helpful to look at bonds, and everything else in our portfolios as well, with a skeptical eye.

My point with all this is that bonds should continue to play an important role in a diversified portfolio, but they require more attention. This is especially true for folks nearing or currently living in retirement because the right bonds act as a store of value while providing current income. And they’re liquid, which is a benefit easily scoffed at until it becomes a problem.

But recent performance and the aforementioned headwinds beg some reasonable questions, like should we jettison bonds in favor of some other asset class? Maybe just have cash in the bank where it’s secure? Or how about preferred stocks, junk bonds, real estate, even crypto?

So over the next few weeks I’ll write up some of my due dilligence work around these questions and share my thinking with you. We’ll look at the case for bonds, which types are best for which situations, and where reasonable alternatives might fit in your portfolio.

Please let me know of any questions and feel free to share your opinions along the way.

Have questions? Ask me. I can help.

- Created on .