Bonds vs Cash

“Today people who hold cash equivalents feel comfortable. They shouldn’t. They have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.” - Warren Buffett

This quote from the Oracle of Omaha pretty much sums up my feelings about holding cash for too long. Yes, it’s immediately gettable and doesn’t come with any market risk like stocks and bonds do. That makes us feel better as Mr. Buffett suggests, but over time the insidious nature of inflation will strip away the purchasing power of that cash and leave you behind the eight ball.

On that note let’s look at our first step in reviewing the investment thesis for bonds in our portfolio. As a reminder, I do this sort of thing regulary but am sharing some of my thinking with you because bonds have been going through a tough time lately. Especially when compared with the stock market, which isn’t really fair but we do it anyway, bonds have been vastly underperforming. So we should review why we own them, compare against alternatives, and then consider what other layers we could add to help performance over time.

This week we’ll look at bonds versus holding cash.

As I mentioned last week, the right kinds of bonds act as a store of value, or something you can trust to put money into today that should, if given enough time, allow for easy access in the future while preserving your purchasing power. In other words, the bonds versus cash question is all about your personal liquidity over different periods of time and keeping up with inflation.

Cash isn’t meant to be held long-term. It’s considered safe because there’s no market risk and is federally insured up to $250,000 per person, per institution, with higher limits possible depending on how accounts are structured. Those are great benefits but the problem is that our economic and financial system incentivizes risk taking, not hoarding cash. We need savers to invest and to put their savings at some amount of risk because this helps keep the economy growing. Savers are rewarded if they do and punished if they don’t. Incredibly low interest rates on cash in recent years has made this painfully obvious.

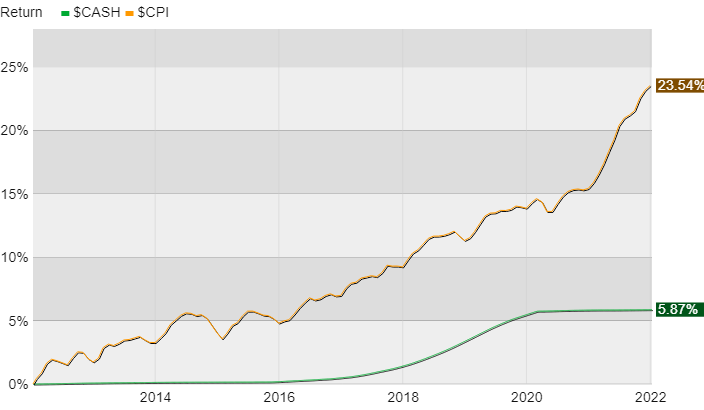

Here’s a chart showing total growth over the last ten years of the Consumer Price Index (CPI) versus the 90-day Treasury bill, a typical proxy for cash. We see that even modest levels of inflation easily degraded cash’s purchasing power. And we all know this has gotten worse lately.

Over longer periods of time cash don’t pay, so to speak. Cash underperformed every other reasonable alternative as well for at least the last 25 years. Again, that’s by design so we should expect this.

That said, having cash at the bank absolutely serves a purpose in the short-term. What’s short-term? Maybe a year or two. My suggestion is to add up what you need for the coming month, add an emergency fund of at least three to six months’ worth of spending, and then add expensive items (appliances, cars, dental work, houses, whatever) you’re pretty sure you’ll want to spend money on in the next year or two. I’d argue that inflation doesn’t matter that much over such a short timeframe. You should willingly pay an opportunity cost to keep this money locked up tight at your local bank or credit union. But beyond that you should do something more productive with your cash.

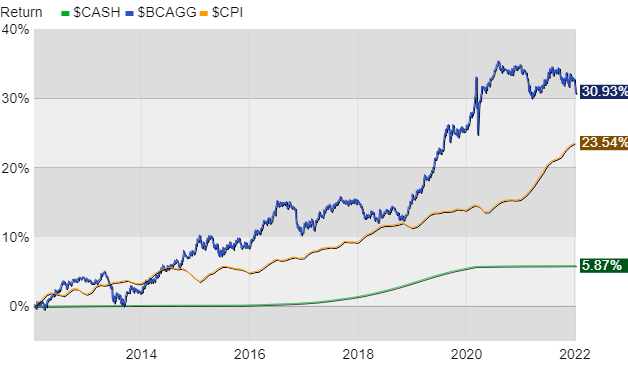

Now let’s add the Bloomberg Barclays US Aggregate Bond index, the main proxy for core (high quality, medium term) bonds, to the chart above. With some exceptions along the way, bond values have maintained purchasing power by keeping pace with the CPI.

With bonds two issues are paramount, credit quality and time. Credit quality, because bonds are loans that borrowers, such as the US Government, states, or US corporations, have agreed to pay interest on before eventually repaying the lender (you). The entity’s ability to do both is measured by its credit rating (good credit = low risk = low interest rates). And time, because the longer you have to wait for repayment, and the longer you’re stuck with a given interest rate, the greater the risk and the more susceptible the bond’s price is to changes in interest rates in the broad market.

I favor core bonds for client portfolios because, again, these bonds act as a medium-term store of cash. The two I use most are the “total bond market” funds from Vanguard and State Street. Both meet the above criteria nicely and have performed as expected, even though they lost money last year. These funds are also inexpensive with an annual cost of about 0.03% compared to an industry average of around 0.5%. And they’re both very actively traded each day, so buying and selling them is easy.

But that’s for the core of your bond portfolio. How about something shorter-term? As I mentioned, holding cash is a good idea up to maybe two years. You can either jump into core bond funds because they also hold short-term bonds, or you could buy a second fund that only owns bonds with shorter maturities. This can work great for stacking, or bucketing, spending needs in retirement.

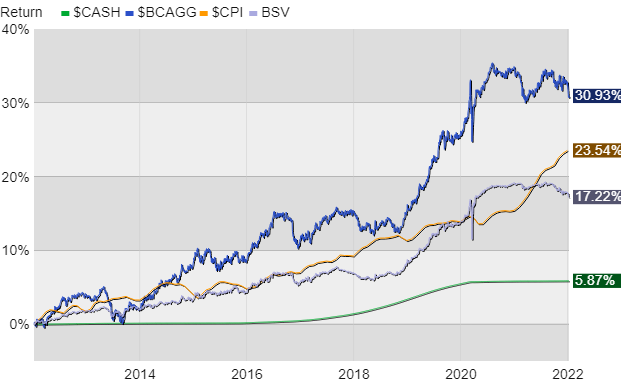

Here’s the same chart but including short-term bonds, in this case Vanguard’s popular index fund, ticker symbol BSV (which I also use sometimes). You’ll see that short-term bonds, the purple line, have lagged the CPI but have still handily outperformed cash.

The bottom line is that bonds pass the test as a store of value while cash doesn’t. Again, I don’t see this relationship changing anytime soon because taking even a little risk is required in our system when thinking out beyond a couple of years. But are bonds the be-all and end-all?

Over the next few weeks we’ll look at reasonable alternatives for bonds and how you might implement them in your portfolio. I don’t want to bore you by looking at everything, so we’ll look at preferred stocks and junk bonds, publicly traded real estate, and perhaps fixed annuities and a little crypto for the sake of variety. If there’s another category on your mind, let me know and maybe we’ll look at that too.

Have questions? Ask me. I can help.

- Created on .