Preferreds and Junk

Before we get to this week’s discussion about bonds, let’s touch on where we are with the stock market right now. It seems like investors can’t buy a positive day lately and that’s quite the harsh entry into 2022 after such great returns last year. That’s one of the things that makes yesterday’s market action so surprising.

The S&P 500 seemed destined to slip into a technical correction as of last Friday, and actually did yesterday before staging a dramatic recovery that saw it and the other major indexes end the trading day positive. (At one point the tech-heavy NASDAQ was down almost 5% but ended up slightly – amazing!) As a reminder, a correction doesn’t start until at least a 10% decline from a recent high. The S&P 500 declines almost 14%, on average, throughout each year in fits and starts, and experiences a technical correction every couple of years, again on average.

Like we discussed before, markets are mostly made up of people, and they’re just as susceptible to mood swings as anyone else. Lately the mood of Mr. Market has been dark and full of foreboding about inflation, whether the Fed can contain it, and what collateral damage might be wrought by the Fed wielding it’s blunt inflation-fighting tool of interest rate increases. There’s even whispers of the dreaded “R” word after some recent economic reports. That, plus any number of other negative headlines in recent days and it’s understandable if investors are feeling glum.

And adding some extra oomph to the gut punch lately is that on many days the stock market was doing fine until the last hour, even the last 15 minutes, of trading. This timeframe is said to be when the so-called smart money makes its decisions. You can tell a lot about institutional investor sentiment by watching what they do during this time. That was when most of the recovery happened yesterday, which was great to see, but it’s tough to watch when it goes the other way.

The bottom line, at least from a purely dollars and cents/market perspective is that corrections are healthy. They shake things up and establish a new price floor from which to keep climbing. That said, it’s very risky to try to “trade” a correction, especially the lightening-fast ones that are typical these days. As of this writing markets are moving lower again, so the mood still seems negative, even after yesterday’s recovery. Lower prices present buying opportunities and there’s a plan in place for that if I’m managing your portfolio. But we want to remain disciplined instead of simply reacting. Reacting is easy so we’ll be content to let others do it.

And, at least in a small way, market volatility like we’re seeing serves to underline points we’re reviewing regarding bonds and the structure of risk in our portfolios. So, with that as a segue, let’s review some alternatives to bonds. This week we’ll look at preferred stocks and junk bonds. We’ll get to others next week.

It’s important to understand where investment options fall on the risk spectrum, pyramid, or ladder (take your pick). Cash is at the bottom (or to one side if it’s a spectrum you’re imaging) and has no immediate risk. It’s followed by short- and then medium-term bonds, and then there’s a giant stride, so to speak, before we get to the options we’ll look at below. Each step up or out adds risk. For this discussion we’re focusing on two main types of risk: default and volatility.

Default risk is exactly what it sounds like (think bankruptcy) and is something to be avoided like the plague. Volatility risk, on the other hand, is more nebulous. It’s the risk of buying the wrong investment (for your situation) at the wrong time, seeing it behave in unanticipated ways, then selling too soon while trying to cut your losses. Time and again this has been a losing strategy accidentally employed by many investors. So we have to pay attention not only to the structure of a fixed income index fund, for example, but also and perhaps most importantly to how it behaves during periods of market turmoil. (As a reminder, bonds are in your portfolio primarily as a longer-term store of value, not exciting growth potential – that’s the job for stocks.)

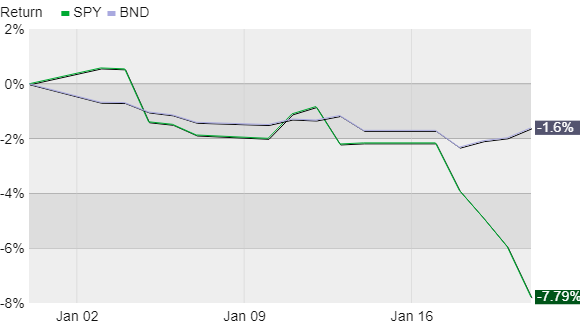

Here’s a chart looking at year-to-date performance of a typical S&P 500 index fund, ticker symbol SPY, compared to Vanguard’s Total Bond Market fund, ticker symbol BND. Both began the year poorly while the bond market ticked up in recent days as the stock market fell. This “flight to safety” isn’t guaranteed, of course, but is a reasonable expectation over time.

Now let’s look at two popular alternatives. The first is an index fund comprised of preferred stocks, ticker symbol PFF. “Preferreds” are considered hybrids of bonds and stocks because they trade like stocks but are in reality a special type of very long-term bond. Companies that issue preferreds pay higher interest rates than they might on traditional bonds they’ve issued because the holders of preferreds (you) have less of a right to repayment if the company defaults.

I’ve always imagined this as waiting in line to be handed pieces of a bankrupt company. Ideally, you’d be first in line or at least near the front. Holders of common stock are last in line. Holders of preferreds are second to last but there can be a long line of traditional bondholders in front of you. What scraps are left when you get to the front? Is it someone’s desk lamp instead of cold hard cash? I’d rather not find out.

In reality, default risk is relatively low when buying a diversified fund like PFF. It currently owns about 500 preferred stocks of companies from a variety of industries. A majority of the holdings are from financial institutions, but the single largest holding is less than 3% of the portfolio. So my main concern isn’t necessarily default risk, it’s volatility risk.

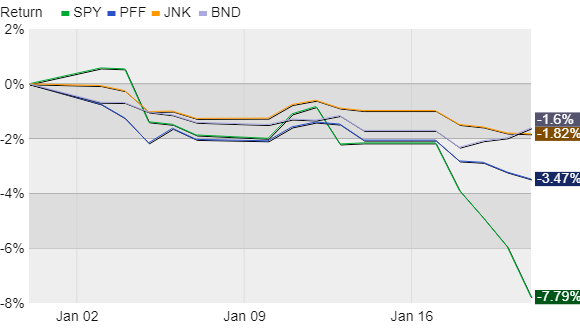

This next chart layers on PFF and the second option we’ll get to in a moment, JNK. Look at how both responded to the recent leg down in the stock market.

JNK is the ticker symbol for a popular high-yield bond fund from State Street. This category of bonds is also referred to using the outdated but functionally accurate term “junk”, hence the ticker symbol.

JNK is a diversified portfolio of bonds from companies with sub-standard credit quality that have to pay higher interest rates to investors. The fund owns many of these bonds across a variety of industries. The top holding is less than half a percent of the portfolio, so the risk of any one company blowing up the fund is essentially diversified away. So again, volatility risk is the main concern when adding this to your portfolio.

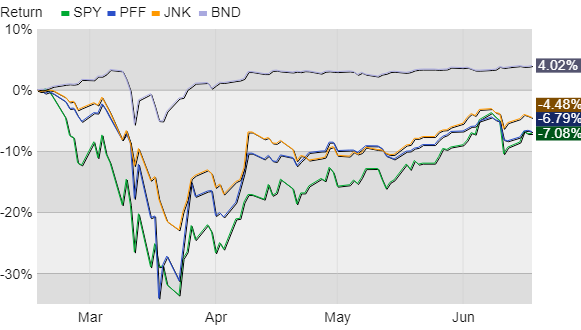

Here’s another chart, but this time I’ve cherry-picked the dates to show you performance during the worst of the initial market reaction to Covid during 2020.

You’ll note that while core bonds fell briefly, PFF and JNK looked more like the stock market. Preferreds tend to act like stocks when investors want to reduce risk and we see that here. Junk bonds also tend to follow this pattern. But junk bonds are still bonds, and bondholders stand before holders of preferreds in that line we’ve discussed, so JNK held up a little better than PFF.

Okay, so what to make of all this? The bottom line is that both of these funds are viable alternatives for a portion of the core bonds in your portfolio. They pay higher interest and that’s great. But you better understand and be prepared for the volatility risk. Here’s an example of what I mean by being prepared before branching out into more exciting fixed income (think of this as an oxymoron).

Cash in the bank = 1 – 2 years of spending (emergency fund + known, or at least likely, big-ticket expenses).

Core bonds = 3 – 6 years of spending if you’re nearing or living in retirement. Maybe more, but I wouldn’t suggest less. Maybe much less if retirement is, say, more than ten years off.

Exciting fixed income (preferreds, junk, etc) = These could round out the rest of your fixed income allocation. Say your top-down allocation calls for 40% in bonds and cash. Back into how much room you have after covering the first two steps above. Maybe a lot, maybe a little. Whatever it is, don’t dip too far into the safe stuff in a reach for yield. If you do, it’s almost Murphy’s Law that you’ll need money and find yourself having to sell losing investments in a down market.

Have questions? Ask me. I can help.

- Created on .