Unhappy Coincidence

Last week ended with a very odd coincidence – stocks, as measured by the S&P 500 and bonds, as measured by the Barclays Aggregate Bond Index, were each down about 10% year-to-date. And that’s for the typical “large cap” stock and “core” bond. Peel back the layers to look at the most growth-oriented stock sectors and longer-term bonds and those assets are close to being down 20% this year. Your average investor doesn’t hang their hat on long-term bonds but still, 20% is a big slide for anything.

The mood in the markets is downright nasty, no way to sugarcoat it. This is unfortunate to say the least given that, from an economic perspective, the consumer is still in decent shape and is actively spending if perhaps not as aggressively as last year. Businesses large and small continue to report good sales numbers (even the airlines are expecting to be profitable this quarter!). And jobs appear to be plentiful. The “headline” unemployment rate, total of those unemployed, and new claims for unemployment are all near pre-pandemic levels. In a perfect world we’d be geared up for more expansion, so why the sudden turn in the markets? One answer is that the stock and bond markets are forward-looking and people (those who run businesses and those who buy from them) across the economy report feeling great about their situation today but express growing pessimism about the future, and that leads short-termers in the market to sell.

There are lots of reasons for this pessimism, from the psychological and the practical to the political, but the biggie is obviously inflation. Last month’s official inflation number was 8.5% and most would agree it’s higher in the real world (or at least it feels that way). According to the Bureau of Labor Statistics, rising gasoline prices made up over half of the headline inflation number. Increased housing costs was also a major contributor. Just about everything we buy costs more now, except for maybe used cars and trucks, at least as of last month. This is unsettling for obvious reasons and absolutely impacts investment decisions.

And now we can add expectations for aggressive Fed policy to the mix. Investors have reacted to this by selling stocks in sectors deemed most sensitive to rising rates and driving down bond prices to adjust to expected rate increases from the Fed. For example, the 2yr Treasury yielded 0.16% a year ago Friday, but investors have sold bonds to the point where the 2yr yield ended last week at 2.72% (now about 2.55% as of this morning). That’s a huge change in the bond world, due entirely to expectations about Fed policy.

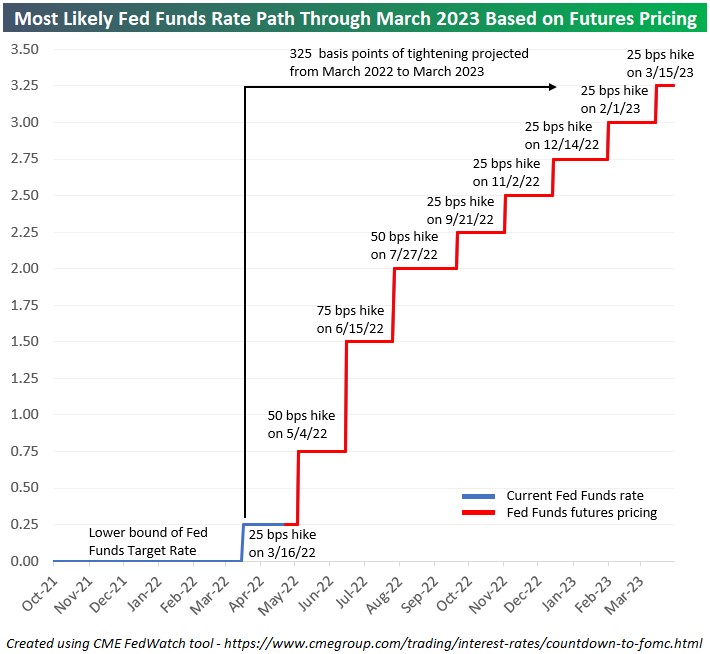

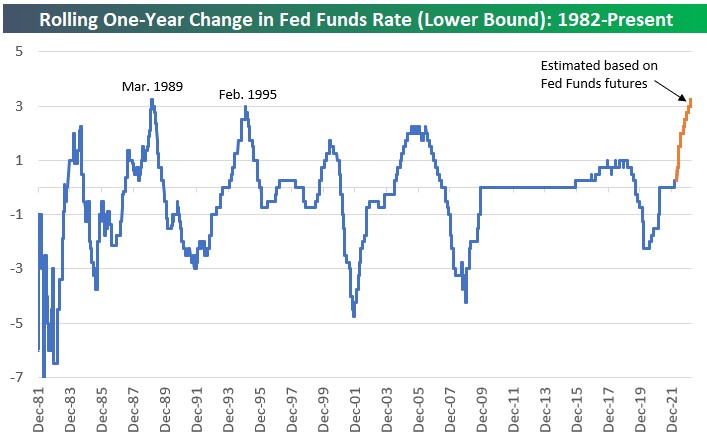

As I’ve mentioned before, bond investors might be getting ahead of themselves here, but overt pessimism continues. According to Bespoke Investment Group, investors are now pricing bonds for a 0.5% rate hike next month, 0.75% in June, and then another 0.5% in July. That would bring the Fed’s short-term benchmark rate to 2.25% this summer from 0.5% now. More rate increases are expected into next year, potentially bringing short-term rates up to nearly 4% in a very short period of time. The following two charts from Bespoke provide a nice visual of investor expectations and a historical comparison. If bond investors are right, this would be tied for the fastest 12-month increase in rates since 1989.

What’s an investor supposed to do about this? Frankly, there isn’t much to do other than ride it out and focus on portfolio structure. If you hold quality bonds in the proper proportions, don’t sell them unless you need to. And consider adding to bonds with extra cash in your portfolio, or rebalancing from stocks to bonds if that makes sense for your situation. You’ll incrementally earn higher yields, and this will help claw back some return.

Beyond that, you could look at adding some alternatives like we discussed in recent weeks. Just be careful to remember that even though prices are down right now, core bonds are referred to in that way because they’re an important part of your portfolio, especially if you’re close to retirement or are living off your savings. Don’t go too far afield while looking for silver bullets because, unfortunately, they don’t exist, no matter what the glossy brochures and infomercials might tell you.

Have questions? Ask me. I can help.

- Created on .