Good morning. We’re ending the quarter this week and I’ve been accumulating several updates to share, so here’s a grab bag of various information.

My website is back up and running. The path of least resistance was to recreate my former site essentially as it was, and I took it, but I’m planning to update the content over the coming weeks.

The Iran War continues and so does its impact on markets. Oil prices had a sustained run over $100 per barrel last week and the global and US oil benchmarks were at about $109 and $105 yesterday afternoon, respectively. Uncertainty about oil prices and potential economic and inflationary impacts have caused stocks to grind lower, as we say, while stocks in the energy sector have done the opposite. Right or wrong, stock prices are on a teeter-totter with oil prices. Positive developments in the war that actually stick have been hard to come by, so it’s anyone’s guess as to how long this situation lasts and what the ultimate impact may be.

However, commodities and interest rate markets are assuming an eventual return to normalcy (whatever that means) and a short-term bout of inflation. A global recession is more likely than it was before the war began, but still generally less likely here at home because our economy is in good shape. Still, we seem to be marching toward a “boots on the ground” incursion into Iran at least as of yesterday, so this is an evolving situation for sure.

Meanwhile, so-called safe haven assets like gold have taken investors on a wild ride in recent weeks, from a high of about $5,400 per troy ounce in late January to around $4,400 last week. Silver has followed a similar pattern. As we’ve covered before, trying to trade this situation or otherwise make big changes to your investment plan is perilous when one “tweet”, “truth”, or whatever term we’re using now can turn markets on a dime. Instead, focus on portfolio structure and other investing fundamentals we can control. And consider treating changes to your portfolio as you would treat decisions about getting tattoos or body piercings, as mentioned recently by The Wall Street Journal’s Jason Zweig. These are major decisions with lasting impact that are hard to reverse, he said, so proceed with caution – sort of an odd example but it works.

Cherry picking timeframes, the S&P 500 dropped about 2% last week and is now down 7% year-to-date through last Friday. The tech sector is down 10%. That’s a technical correction for the sector and a quick reversal of the 7% YTD gain we saw as recently as late February. Developed foreign and emerging markets have been faring worse since Operation Epic Fury began on Feb 28th, especially Asian markets because of more exposure to Middle East oil. But in general, foreign markets are still ahead of us YTD due to better performance earlier this year. These timeframes are arbitrary, but the comparison is still worthwhile as a quick check on our position. Here’s another: the S&P 500 is up about 13% going back 12 months, 66% for three years, with Tech up 23% and 83% over the same timeframe. Foreign markets have also done well over these timeframes that include a variety of shocks. My point is that while this is a challenging time, we’ll get through it.

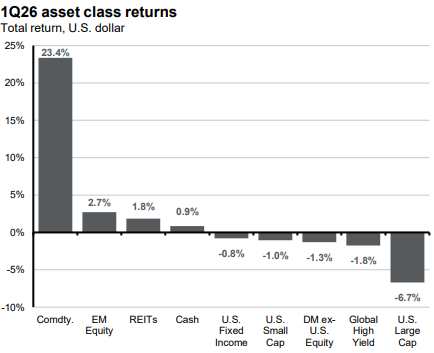

A reminder and interesting chart from JPMorgan this morning showing the lopsided returns so far this year… Last year’s rocky start [caused by the so-called Tariff Tantrum in early April 2025] faded quickly, with markets finishing strong — a reminder that in markets, winters are often short and summers long. Therefore, investors would be wise to use the recent dislocations in the market to position portfolios for structural growth themes that are likely to persist long after the conflict in the Middle East is resolved.

The economy is facing risk from higher oil prices but went into this war on a solid footing. Corporate earnings were/are strong across sectors and the AI race, with all its potential issues, continues. The US consumer remains healthy, at least on average. The higher-end consumer is doing great while the lower-end is getting squeezed. For example, there are reports of a large uptick in 401(k) plan hardship withdrawals last year. Congress made taking these easier within the OBBBA and that might be part of the issue, but it’s one of many indicators of stress at the lower end of the economic food chain. Toward the other end, one example comes recently from Delta Airlines, whose CEO reported record-breaking bookings in March with an emphasis on premium seats. Maybe some of this was frontrunning expectations for higher ticket prices due to rising oil prices, but more affluent consumers still showed the demand and had the money to buy more expensive seats, right? And this isn’t a new trend; airlines have been reporting better bookings for premium seats than for economy seats for a while now. That’s not the whole economic picture, of course, but strong consumption from one side of the wealth gap helps keep our economy afloat.

Interest rates on cash and bonds are in motion. I mentioned last week how it’s important to keep your short-term money working as hard as it can. Along those lines, yields on bank CDs have risen lately. I’m seeing around 3.9% in the Schwab system for various banks and maturities going out from a few months to two years. This is up nearly a quarter point. Some online banks via www.bankrate.com are offering 4% to 4.1% for nearly a year. Short-term Treasuries are slightly lower than this. Money market mutual funds at Schwab and elsewhere are a tad lower as well because their yields don’t respond as quickly, for better or worse. And medium-term bond yields rose to nearly 4.5% last week. These rate changes present an opportunity to review your cash position.

I’ll have my regular Quarterly Update next Tuesday. Enjoy the rest of your week!

Have questions? Ask us. We can help.