Tax season is always hectic for taxpayers and the professionals who help them: details, deadlines, and often negative surprises. Recent law changes exacerbated this dynamic. Still, numerous taxpayers have been pleasantly surprised at the size of their refunds this year.

The Tax Foundation reports that as of late March refunds averaged about $3,500 and are up about 11%, or around $350, from last tax season. I’ve read elsewhere this might end up being around a 20% increase by the time tax season is over if you factor in overall lower tax bills from greater deductions, not just refund amounts.

We’ll leave the how’s and why’s of this for another day, but one interesting aspect of increased refunds is who’s receiving them and how this might help offset rising gas prices due to the Iran War.

Nationally, gas and diesel prices have jumped 30+% since the war began. Rapid price increases in something so ubiquitous are bad for the economy but can be offset by price decreases for other items and/or reduction in demand. That’s obviously challenging when it comes to a global economy that runs overwhelmingly on fossil fuels. So, economists are digging through the weeds trying to reconcile the jump in gas prices with an economy, at least here at home, that is doing pretty well.

Consumer prices across the economy, measured by various metrics including so-called headline inflation that includes energy prices, were up 3.3% in March compared to a year ago. Gasoline prices made the largest impact on the headline inflation numbers released last week, rising nearly 19% since last March. This was followed closely by airfares, which were up almost 15%. Otherwise, price increases would have averaged out modestly across the economy to a relatively benign 2.6% instead of 3.3% if we excluded energy.

Overall, that’s a big jump from February’s 2.4% annual rate. Most economists and analysts see this as a short-term issue and aren’t expecting a recession specifically from this. But it’s easy to imagine them getting more nervous as the days tick by without a meaningful resolution to the war that allows for the free flow of trade through international waters. One can only hope that reports of a new round of peace talks later this week bears fruit. Because add on a couple more months of this and it’s a different story when it comes to recession risk. In the meantime, lots of people are watching to see how the various parts of our economy can absorb higher fuel prices and if consumption from wealthier households continues to be the tide lifting all boats.

Along these lines I wanted to share a piece from JPMorgan that I received yesterday…

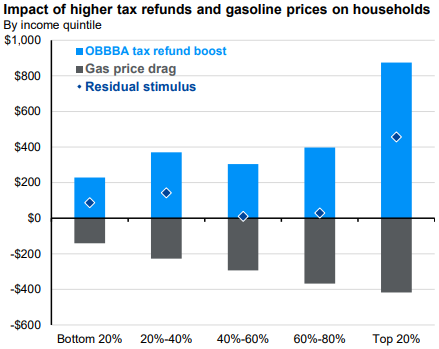

Coming into 2026, investors were enthusiastic that fiscal stimulus from the One Big Beautiful Bill Act (OBBBA), particularly larger income tax refunds, would boost growth. The good news is that we estimate the average income tax refund will increase by $400 from 2025.

However, there is some bad news. Energy prices are spiking due to the conflict in the Middle East. Regular retail gas prices have averaged $4.13 so far this month, up from $2.93 in February and $3.19 last April. This has raised concerns that higher gas prices could offset larger income tax refunds. Higher gas prices should only partially offset stimulus from income tax refunds, but the extent varies by income cohort. The top 20% of households consume the most gasoline (~1,000 gallons in 2024) but also benefit most from larger refunds since most OBBBA tax breaks come as deductions. Higher gas prices offset 48% of the refund benefits for this cohort, while lower income households could feel more pressure.

More than 90% of the tax refund boost for middle-to-upper-middle income households could be offset by higher gas prices, and 62% for the bottom two quintiles. There are some important nuances to consider.

The Middle East conflict is impacting more than just gas; the outlook for energy prices remains uncertain; and the timing of higher energy costs and tax refunds may not align. Moreover, tax savings can manifest as lower tax bills, not just larger refunds.

That said, higher gas prices appear likely to only partially negate the stimulative impacts of larger refunds, with upper income households faring best. With that cohort responsible for an outsized share of spending, the energy price shock alone should not topple the U.S. economy into recession. However, the Administration may feel tempted to pass additional stimulus ahead of midterm elections.

Have questions? Ask us. We can help.